Issue #201:

BTC Finally Breaks Out… But For How Long?

Markets Driven by Momentum, Constrained by Uncertainty

With Bitcoin moving decisively above range highs last week and closing near $74,000, we finally breached an important technical level. However, the rally was largely mechanical, driven by a $530 million short squeeze triggered by the current geopolitical news agenda and sustained institutional spot absorption.

Beneath the surface, three shifts are reshaping the market outlook. Firstly, altcoins have finally shown rotation, with the TOTAL2 index testing a three-month high as Ethereum outperformed and on-chain activity surged, marking the first move in tandem with BTC since January. Secondly, positioning has diverged sharply, institutions are hedging via puts on CME, while speculative flows on Deribit remain aggressively long. Finally, the near-term trajectory now hinges on geopolitics. If the US-Iran ceasefire deadline expires on 21 April without resolution, upcoming negotiations represent a binary catalyst that could determine whether this breakout evolves into continuation, or failure.

In the meantime, the macro economy continues to look uncertain. The US housing market is beginning to weaken as higher mortgage rates, inflation, and declining consumer confidence weigh on demand, pushing existing home sales to a nine-month low and dampening builder sentiment. Although rising inventory and stable employment suggest a gradual rebalancing rather than a sharp downturn, affordability constraints and economic uncertainty are likely to keep activity subdued in the near term.

This softening in housing aligns with broader macro trends, where inflation remains elevated even as demand begins to slow. Producer prices continue to rise due to higher energy and domestic costs, while import price pressures are easing, indicating that inflation is shifting from global supply factors to internal cost pressures. As businesses face tightening margins and consumers become more price-sensitive, the economy is entering a slower growth phase, leaving the Federal Reserve navigating a complex balance between persistent inflation and weakening momentum.

The digital asset landscape is also evolving evidenced by enforcement, regulation, and institutional adoption, highlighting both progress and persistent challenges. In the United States, authorities have launched a claims process to compensate victims of the 2014-19 OneCoin fraud, allowing eligible investors to recover funds from a pool exceeding $40 million, only a fraction of the estimated $4 billion lost globally. While this marks progress in accountability, it underscores the limitations of recovering losses from large-scale, cross-border crypto fraud.

At the same time, regulatory frameworks are advancing. Pakistan has moved to integrate crypto into its financial system by permitting banks to service licensed virtual asset firms under the Virtual Assets Act 2026. The approach remains cautious, with strict compliance requirements and restrictions on direct crypto exposure, signalling a shift from suppression to controlled adoption.

In parallel, institutional participation is accelerating in developed markets. Charles Schwab’s rollout of its spot crypto trading platform enables clients to trade Bitcoin and Ethereum alongside traditional assets, reflecting deeper integration between traditional finance and digital markets.

Market Signals

Altcoin Awakening as Range Breakout Holds…For Now

Bitcoin started last week strongly, posting a 5.2 percent advance on Monday, April 13th, and decisively confirming a breakout above established range highs. The weekly close was registered near $74,000, capping off a five-day sustained ascent from the Monday low of $70,470 to a Friday peak of $78,328, an 11 percent peak-to-trough price fluctuation in a single trading week. The price then slightly retraced as the US-Iran ceasefire seemed to end and speculative positioning ahead of the new week came in.

Figure 1: BTC/USD Daily Chart. (Source: Bitfinex)

Crucially, this pronounced rally was not driven by typical market dynamics but was instead engineered by two distinct mechanical forces:

- A Short Squeeze Event: A cascade of aggregate short liquidations totaling $530 million was triggered following the announcement on April 13 of a US naval blockade of the Strait of Hormuz.

- Sustained Institutional Absorption: The consistent Strategy STRC-funded spot absorption programme exerting upward pressure on price. This persistent buying has elevated corporate treasury holdings overall to 780,897 BTC, and correlated with STRC experiencing record trading volumes.

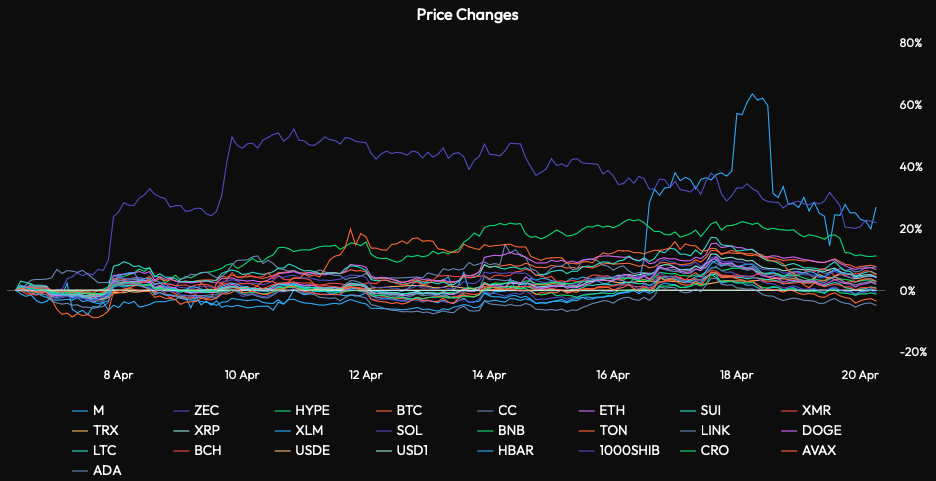

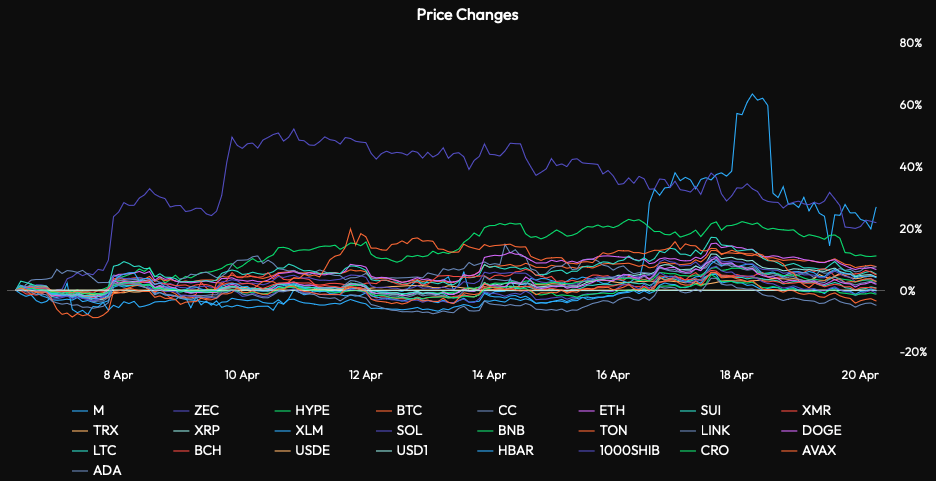

Three distinct behavioural shifts defined the past week, presenting a divergent outlook for the market. Firstly, the altcoin market finally exhibited rotation. TOTAL2 (crypto market capitalisation excluding BTC) surpassed $1.04 trillion, crucially testing a three-month range high.

Figure 2: Total Market Capitalisation. (Source: CryptoCap)

This move was driven by Ethereum’s 280 basis point outperformance against BTC, and a 41 percent week-on-week increase in on-chain activity, marking the first significant alt rotation since range-bound trading began in January.

Last week was the first time alts moved in tandem with BTC, while some select tickers moved aggressively higher. Indeed, an interesting finding across relative price movements is that a majority of large caps have continued to underperform in BTC terms. And the ones that have continued to exhibit relative strength, namely, ZEC and HYPE, always do so after BTC has had its initial leg up.

Figure 3: Large Cap Altcoins Price Movements Against Bitcoin Over The Past Two Weeks.

Secondly, institutional options positioning has become notably decoupled. CME open interest shows a heavy bias towards puts, indicative of institutional hedging, with Deribit registering a 56.8 percent call dominance, suggesting speculators are aggressively pressing long positions.

Thirdly, a significant geopolitical deadline looms: the ceasefire clock expires tomorrow, 21 April, and looks like it will do so without a formalised framework. This means the second round of Pakistan-mediated talks represents a binary catalyst for the market’s next directional move.

General Macro Update

US Housing Market Weakens

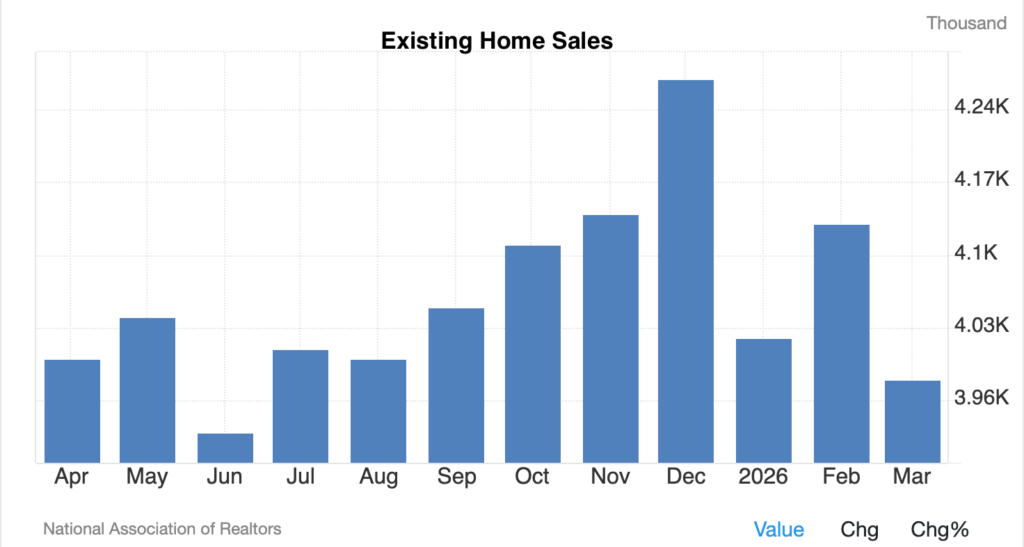

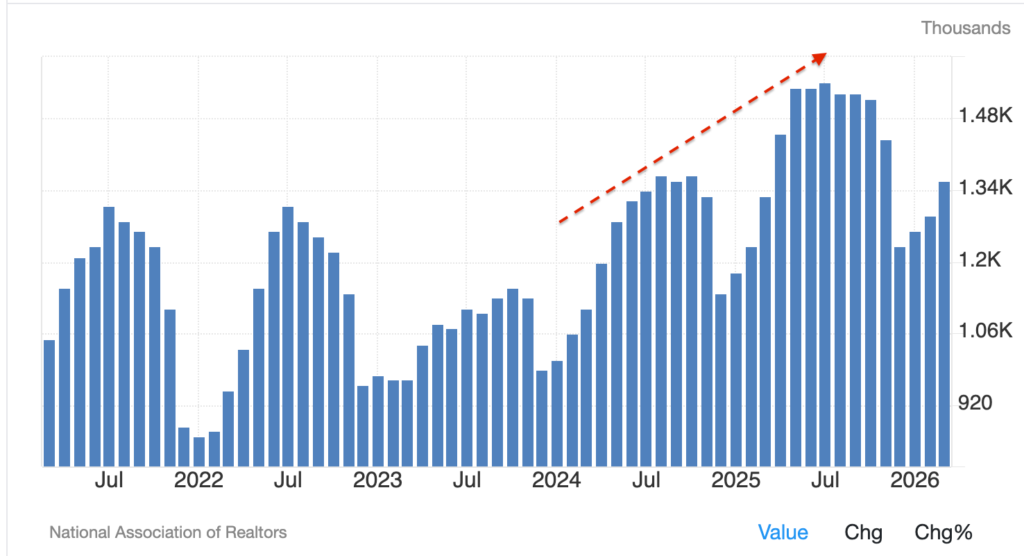

Figure 4: Existing Home Sales (Source: National Association of Realtors)

The US housing market is showing signs of strain as rising mortgage rates, weaker sentiment, and geopolitical tensions reduce both buyer activity and builder confidence. While supply conditions are slowly improving, affordability challenges and economic uncertainty continue to limit a sustained recovery.

Data from the National Association of Realtors showed that Existing Home Sales declined to a nine-month low in March, reflecting weaker demand across all regions. The report highlighted how rising mortgage rates and declining consumer confidence are affecting purchasing decisions, despite earlier improvements in affordability. Existing home sales fell 3.6 percent to an annual rate of 3.98 million units, indicating that contracts signed earlier in the year did not translate into sustained market momentum.

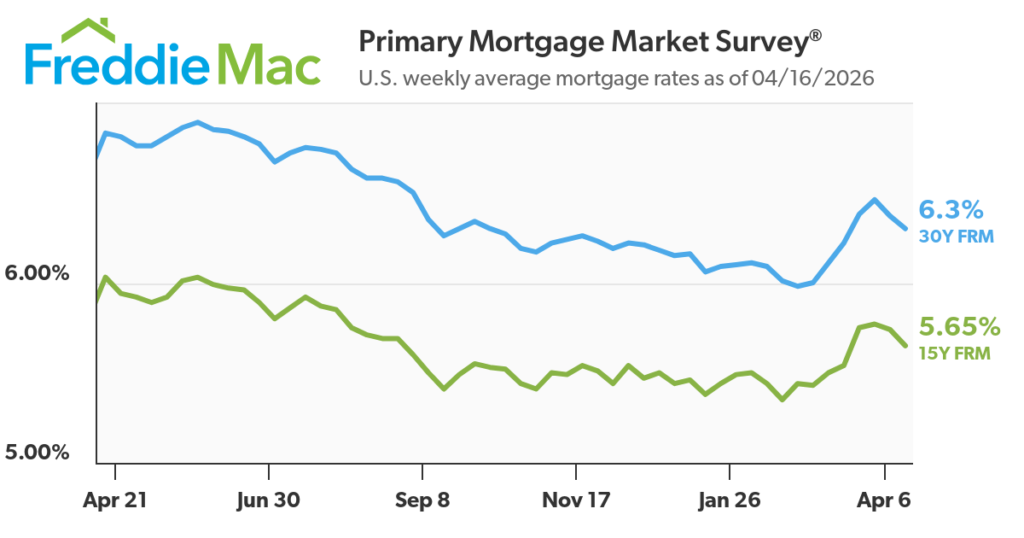

Figure 5: Freddie Mac 30-Year and 15-Year Fixed Rate Mortgage

The increase in borrowing costs has been a key factor. The 30-year fixed mortgage rate rose from 5.98 percent in late February to above 6.3 percent in April, following higher US Treasury yields driven by inflation concerns. Rising energy prices linked to geopolitical tensions have intensified the pressure on inflation, and in turn reduced household purchasing power and increased the cost of homeownership.

At the same time, builder sentiment has weakened. The National Association of Home Builders/Wells Fargo Housing Market Index fell to 34 in April, marking a seven-month low and below the neutral threshold, where it has languished for nearly two years. Builders reported rising material costs, driven in part by higher fuel prices and supply disruptions, alongside continued labour constraints. These cost pressures have made it more difficult to price homes and have reduced the use of incentives to encourage buyers, signalling a more cautious approach to new construction.

It’s Not All Gloom

Figure 6: Housing Inventory in the US

(Source: National Association of Realtors, Trading Economics)

Despite these challenges, underlying market dynamics suggest a gradual rebalancing rather than a sharp downturn. Housing inventory has increased for 28 consecutive months, providing buyers with more options, while home prices have risen modestly year over year. Demand indicators, such as online listing views, remain elevated, though many households are delaying purchases due to uncertainty around employment and future costs.

Macroeconomic conditions, however, continue to shape housing activity. Inflation has accelerated to 3.3 percent, largely driven by a sharp increase in energy prices, while the Federal Reserve has maintained interest rates within a 3.5-3.75 percent range. Although the labour market remains relatively stable, with steady job creation and unemployment at 4.3 percent, concerns about job security and declining sentiment are weighing on consumer behaviour.

Looking ahead, the housing market is expected to remain subdued in the near term. While improving inventory and gradual affordability gains could support activity later in the year, elevated mortgage rates and broader economic uncertainty are likely to limit a rapid recovery. As a result, the market is transitioning into a more balanced state, where supply and demand adjust gradually rather than through abrupt price movements.

Inflation Growing as Demand Slows

Upstream inflation remains elevated even as external price pressures begin to ease, creating a mixed macro environment for policymakers. While businesses continue to face rising input costs, broader economic activity is showing signs of slowing, complicating the Federal Reserve’s policy outlook.

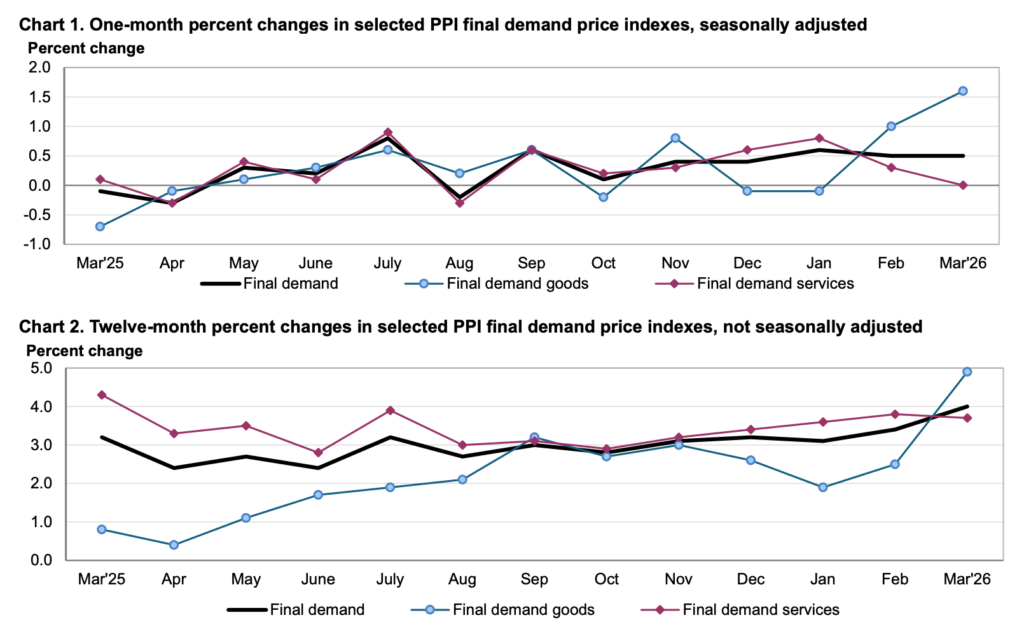

Figure 7: Yearly and Monthly Percentage Change in US Producer Price Index

(Source: US Bureau of Labour Statistics)

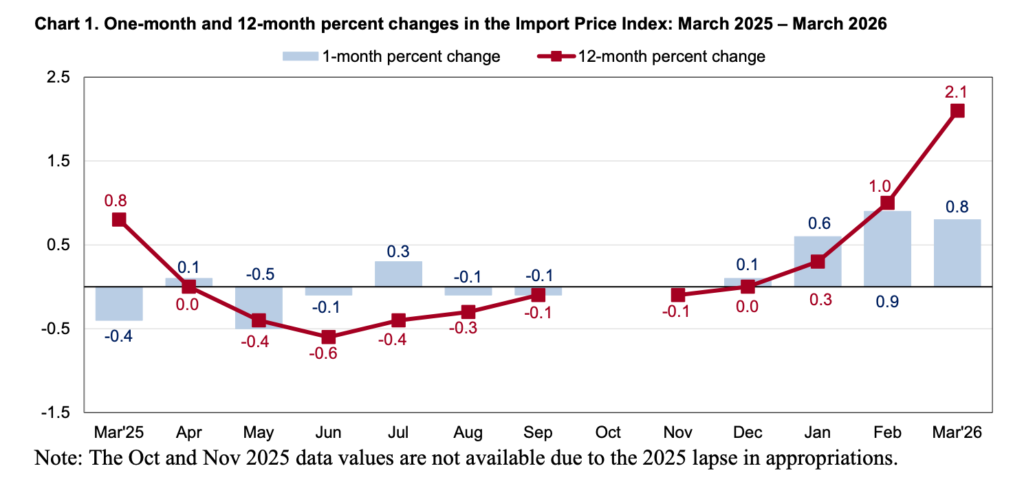

In March, the Producer Price Index (PPI) released by the US Bureau of Labour Statistics (BLS) rose 0.5 percent month-on-month and 4 percent year-on-year, indicating that production costs remain firm despite coming in below expectations. At the same time, the Import Price Index also published by the BLS increased 0.8 percent over the same period, suggesting that price pressures from overseas goods are rising at a slower pace than forecast. Together, these indicators provide insight into inflation at different stages of the supply chain, PPI reflects domestic production costs, while import prices capture the cost of foreign inputs entering the economy.

The divergence between these two measures highlights the evolving nature of inflation. Higher energy costs, driven by geopolitical tensions in the Middle East, have lifted domestic production expenses, particularly in fuel and transportation. This has kept PPI elevated, as businesses pay more to produce and distribute goods.

However, the slower increase in import prices suggests that external inflationary pressures are beginning to moderate. In simple terms, while global supply costs are stabilising, domestic cost shocks – especially energy – are still feeding into the economy.

Figure 8: Change in Import Price Index (Source: Bureau of Labour Statistics)

This dynamic creates a challenge for businesses. Firms are experiencing rising input costs but are increasingly unable to pass these costs on to customers. As a result, profit margins are tightening. This aligns with broader economic observations from the Federal Reserve’s latest Beige Book, which reports that input costs are rising faster than selling prices across multiple regions. Businesses are therefore absorbing a greater share of inflation rather than transferring it fully to consumers.

The Beige Book also indicates that economic activity is expanding at a modest pace but losing momentum. Consumer spending remains positive but uneven, with lower-income households showing greater price sensitivity. Meanwhile, the labour market is stabilising, with cautious hiring and limited wage growth. These conditions suggest that demand is not strong enough to sustain aggressive price increases, even as cost pressures persist.

Energy remains the central transmission channel across all three data points. The surge in oil prices has increased production and transportation costs, directly lifting PPI. It has also contributed to broader uncertainty, influencing business investment decisions and consumer confidence, as reflected in the Beige Book. This reinforces the idea that current inflation is being driven more by supply-side shocks than by strong demand.

For the Federal Reserve, this presents a complex policy trade-off. On one hand, easing import prices and moderating consumer inflation suggest that overall price pressures may be stabilising. On the other hand, persistent cost-driven inflation and fragile economic growth limit the scope for immediate policy easing. The Beige Book’s characterisation of a “cautious expansion” indicates that the economy is entering a late-cycle phase, where growth slows, but inflation risks remain.

The combination of firm producer prices, moderating import costs, and a slowing but resilient economy suggests that inflation is shifting rather than disappearing. The Federal Reserve is likely to remain data-dependent, balancing the risk of entrenched cost pressures against weakening economic momentum.

News From the Cryptosphere

Claims Process Opens for OneCoin Fraud Victims

The US Department of Justice initiated a formal claims process to compensate victims of the notorious OneCoin scheme, widely regarded as one of the largest cryptocurrency frauds in history. The program enables eligible investors who suffered losses between 2014 and 2019 to seek restitution from a pool of more than $40 million in assets recovered through criminal forfeiture. While the initiative marks a significant legal milestone, it represents only a fraction of the estimated $4 billion lost globally, highlighting the structural limitations of post-fraud recovery mechanisms.

OneCoin, founded by Ruja Ignatova and Karl Sebastian Greenwood, operated as a global multi-level marketing scheme disguised as a cryptocurrency project. Despite marketing itself as a rival to Bitcoin, the platform lacked a legitimate blockchain infrastructure, relying instead on fabricated narratives and aggressive network-driven sales tactics to attract millions of investors worldwide.

The newly launched remission process, administered by a third-party claims handler, requires victims to submit petitions by June 30, 2026. Eligibility is restricted to individuals who can demonstrate net losses from purchasing OneCoin during the scheme’s operational period. Authorities have emphasised that the compensation fund is derived solely from seized assets linked to prosecuted individuals, with ongoing efforts to trace and recover additional proceeds.

Despite multiple convictions, including Greenwood’s 20-year prison sentence, the case remains partially unresolved, as Ignatova, often referred to as the “Cryptoqueen,” remains at large. The DOJ’s move underscores both the progress made in dismantling large-scale crypto fraud networks and the enduring challenges of delivering meaningful restitution in globally distributed financial crimes.

Pakistan Opens Banking Rails to Crypto Firms

Pakistan has taken a decisive step toward integrating digital assets into its formal financial system, by permitting banks to provide services to licensed virtual asset service providers. This move effectively reverses a longstanding 2018 restriction that had isolated crypto-related businesses from the traditional banking sector.

The policy shift follows the enactment of the Virtual Assets Act 2026, which establishes a comprehensive legal and regulatory framework for digital asset activity in the country. Under this regime, only firms licensed by the Pakistan Virtual Assets Regulatory Authority are eligible to access banking services, ensuring that participation in the ecosystem is subject to oversight, compliance, and standardised governance.

Despite opening banking access, the framework remains deliberately conservative. Financial institutions are required to conduct strict due diligence, comply with anti-money-laundering protocols, and maintain segregated, non-interest-bearing accounts for client funds. Crucially, banks are prohibited from directly holding or investing in crypto assets, reflecting a regulatory approach that enables access while containing systemic risk.

This development represents Pakistan’s first formal attempt to bring crypto activity under regulated financial rails rather than suppress it. Policymakers are positioning the shift as foundational, transforming the sector from an informal, high-risk environment into a supervised part of the broader economy.

Beyond domestic implications, the move signals Pakistan’s ambition to participate more actively in the global digital asset ecosystem. With parallel initiatives such as partnerships for asset tokenisation and exploration of stablecoin-based payments, the country is gradually transitioning from regulatory ambiguity toward structured adoption, balancing innovation with financial integrity in a rapidly evolving market.

Charles Schwab Enters Spot Crypto Trading

The US brokerage, Charles Schwab, has begun rolling out its long-anticipated spot cryptocurrency trading platform, branded “Schwab Crypto”.

The platform will enable clients to directly buy, sell, and hold Bitcoin and Ethereum, and is being introduced in phases, initially granting access to employees and select users before expanding to the broader client base.

Integrated across Schwab’s core platforms—including its flagship trading interface and mobile ecosystem—the service allows investors to manage crypto alongside traditional assets such as equities and bonds, reinforcing a unified portfolio experience.

From an infrastructure standpoint, the platform leverages a hybrid custody model: assets are held through Schwab’s banking arm, while blockchain infrastructure, trade execution, and sub-custody are handled by Paxos. This structure reflects a compliance-first approach, aligning crypto exposure with established financial safeguards.

Fee positioning is equally strategic. Schwab has set transaction costs at approximately 0.75 percent per trade, competitive relative to incumbents like Fidelity, while eliminating custody fees, signalling an effort to attract cost-sensitive retail and institutional participants.

Ultimately, the launch represents more than a product expansion; it is a structural convergence of traditional brokerage infrastructure with native crypto markets. With trillions in client assets and a deeply entrenched retail base, Schwab’s entry is poised to accelerate mainstream adoption, reinforcing a broader trend in which legacy financial institutions transition from passive gateways to active participants in the digital asset economy.