Issue #208:

BTC Slides as Real Yields Climb

Inflation Drives Repricing Across Risk Assets

Bitcoin has broken decisively into a deeper corrective phase, printing a multi-year low at $59,200 on June 5th and extending its drawdown to 53 percent from the October 2025 all-time high. The move has been driven by a combination of record ETF outflows, derivatives deleveraging, and a persistently restrictive macro backdrop, with the 10-year yield above 4.45 percent and Fed expectations shifting back toward higher-for-longer policy.

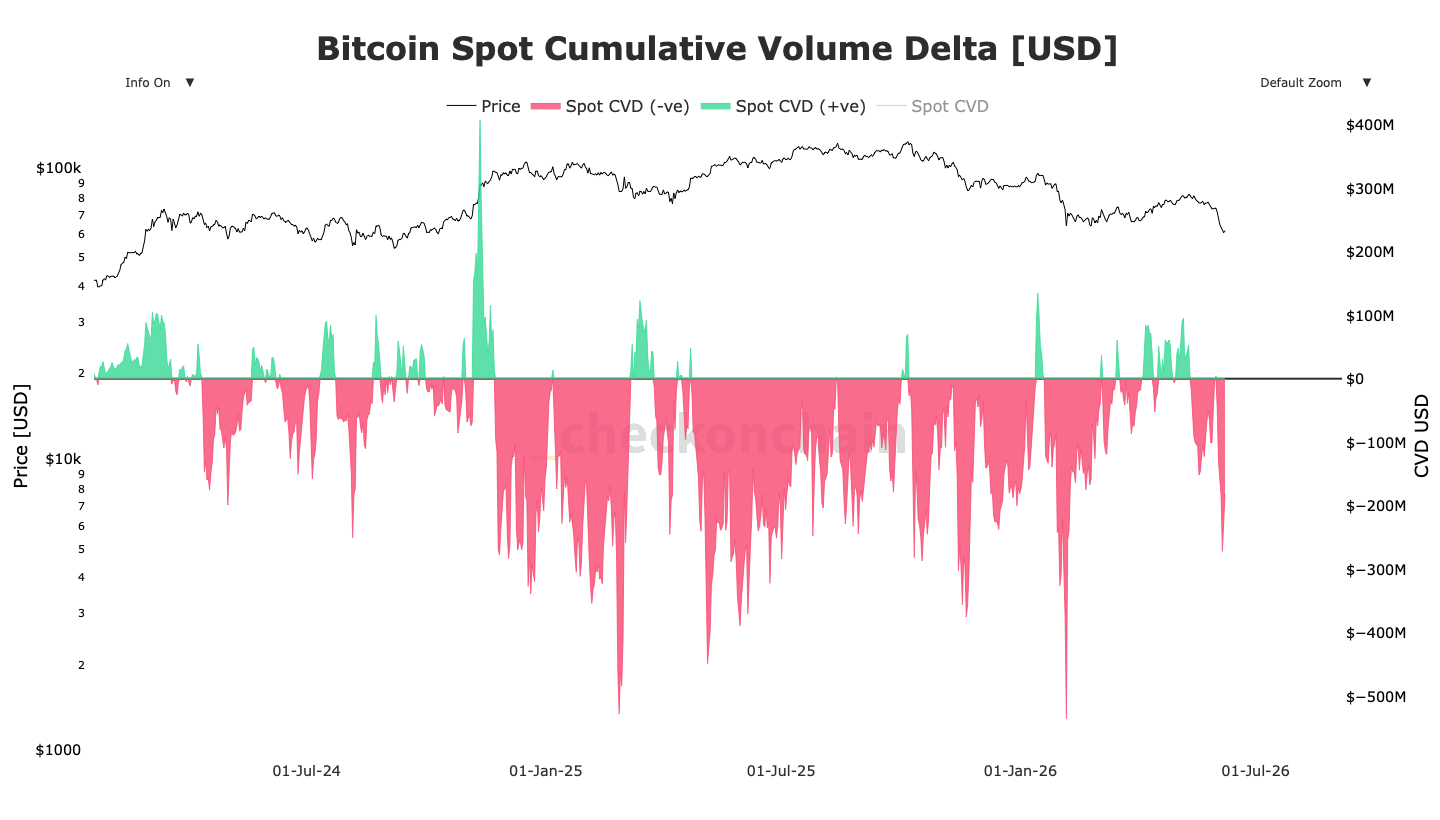

Both on-chain and flow data reinforces the view that this is a distribution-heavy regime rather than a clean capitulation. Spot Cumulative Volume Delta has turned sharply negative after a strong April–May accumulation phase, indicating that recent buyers are now actively exiting into weakness. The Short-Term Holder cost basis has broken below the True Market Mean ($77,800), confirming that newer entrants are underwater and adding overhead resistance into every rebound. With price now drifting toward the broader realised cost basis near $53,900, rallies are increasingly being sold rather than accumulated, signalling that the market remains in a structurally defensive phase until spot demand meaningfully returns.

The macro data shows an economy that is still growing, but losing ground to inflation, which is where it matters most to households. The labour market firmed up after a soft start to the year: job openings reached their highest level in nearly two years, payroll growth held above the replacement rate, and hiring broadened into healthcare, manufacturing, construction, and leisure. Layoffs stayed low and retention stayed high. Business investment, led by AI infrastructure, continued to support activity and corporate margins. The problem is inflation. Prices are set to outrun wages, so real incomes are falling even as nominal pay rises. That leaves the Federal Reserve balancing a healthy jobs market against inflation still well above target, and it frames the second half of 2026 as a contest between steady employment and shrinking purchasing power.

That same inflation is now driving markets. Treasury yields are rising on an inflation premium rather than on stronger growth expectations, pushed by higher energy prices and renewed geopolitical risk. As oil climbs, inflation expectations climb with it, lifting nominal and real yields and tightening conditions across asset classes. Higher real yields raise the cost of holding anything that does not generate income, and investors have started repricing risk accordingly. Bitcoin is the clearest case: US spot ETF flows reversed sharply, producing the largest outflows since the products launched and a sharp drop in price. The market has stopped pricing rate cuts and started pricing the risk that policy stays restrictive for longer. For now, the path of real yields is the single most important driver of both traditional and digital assets.

Underneath the macro pressure, the institutional build-out of crypto continues. Securitize’s clearance to list on the New York Stock Exchange takes tokenisation infrastructure public and makes it an investable asset in its own right, closing more of the distance between traditional finance and on-chain markets. Stablecoins are moving in the same direction as the government finalises the GENIUS Act, which holds issuers to the compliance standards of regulated financial institutions. Bitcoin’s institutional market is maturing too. Record ETF outflows and Strategy’s turn toward disciplined balance-sheet management look like ordinary portfolio decisions, not a loss of conviction. The through line is that digital assets are being absorbed into the financial mainstream, subject to the same supervision, macro forces, and allocation calls as everything else.

Market Signals

The Floor Beneath The Floor

On June 5, Bitcoin hit a multi-year low of $59,200, marking its weakest valuation since October 2024, and representing a 53 percent drawdown from the October 2025 all-time high, and a 28.5 percent decline from the recent highs hit in mid-May. The once-solid $60,000 floor, which has anchored price action since February, was lost on significant volume.

Following the June monthly open at $73,750, the market has retreated into its Q1 2026 consolidation zone, shedding more than 20 percent in the process. Rather than a technical pullback, the early June move signals at best an acceptance of BTC in a range between $60,000 and $72,000, and at worst a shift toward price discovery at levels not visited since the maturation of the spot ETF market.

The worst case scenario will play out if BTC breaks through $60,000 for a sustained period of time. For now, price is stalling near previous range lows. The entire move has been propelled by three primary catalysts: historic ETF outflows alongside Strategy’s pivot to managing dividends via bitcoin sales (where market sentiment outweighs the actual volume sold), a significant deleveraging in derivatives markets, and a hawkish macroeconomic environment. Conversely, a resilient supply base suggests that capitulation has not yet occurred.

Persistent macroeconomic headwinds, headlined by the 10-year Treasury yield climbing past 4.45 percent and job openings hitting a two-year peak, have forced a repricing of Federal Reserve expectations. Fed futures markets have abandoned forecasts for policy easing this year, instead assigning a 50 percent

probability of a further rate hike. This shift has driven prices sharply away from the True Market Mean of $77,800, a level representing the cost basis of active supply, and a historical divider of market cycles, and toward the Realised Price at $53,900, which marks the aggregate acquisition cost of all circulating supply. This rejection of the True Market Mean validates the continuation of the current bear market regime.

Notably, the Short-Term Holder Cost Basis at $76,400 has dipped below the True Market Mean for the first time since January 2022. This alignment suggests that recent market entrants are building positions beneath the core valuation anchor, a characteristic of mature bear cycles where the duration of the drawdown erodes investor sentiment. Historically, such conditions increase the likelihood of structural exhaustion or significant liquidations among large-scale participants. Spot Cumulative Volume Delta Goes Negative

Activity within the spot markets has seen a marked degradation throughout the previous fortnight. Spot Cumulative Volume Delta has transitioned into a clear negative regime (see Figure 3), touching depths reminiscent of the large liquidations seen in February. The data confirms that aggressive distribution, especially by recent buyers, is currently the dominant force on exchange order books.

The current shift is particularly significant given the backdrop of robust, spot-driven accumulation that characterised the market during April and the initial weeks of May. Throughout that period, the bid side of the book was consistently active, pushing Spot Cumulative Volume Delta into positive territory and facilitating Bitcoin’s ascent from the mid-$60,000 range toward the $80,000 threshold. That bullish impulse has evidently exhausted itself, as market participants failed to find sufficient momentum for a breakout, allowing sellers to re-establish control.

Historically, a sustained period of negative Spot Cumulative Volume Delta aligns with either the final stages of investor capitulation or the inaugural phase of a structural trend pivot. The present environment leans towards a market firmly entrenched in a distribution cycle, where spot participants are opting to sell into strength during intermittent rallies rather than adding to positions. A fundamental reversal in spot demand dynamics remains a necessary precursor for any sustainable recovery in valuation.

General Macro Update

US Labour Market Remains Resilient, But Inflation Risks Threaten Real Wage Growth

The labour market continues to be a rock of stability in the US economy. After a short period of weakness, hiring has recovered and job openings are now at their highest levels since 2024. However, persistent inflationary pressures and rising costs across key sectors could undermine household purchasing power, creating challenges for both consumers and policymakers in the second half of 2026.

Hiring Recovers as Job Openings Reach a Two-Year High

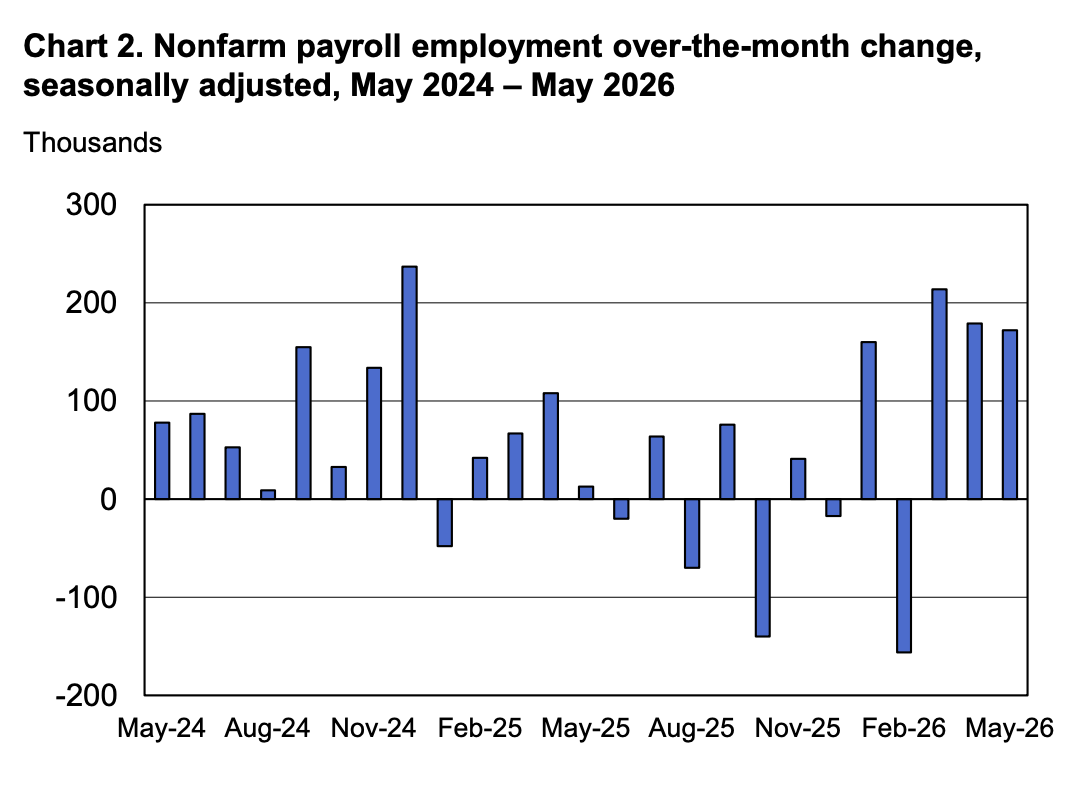

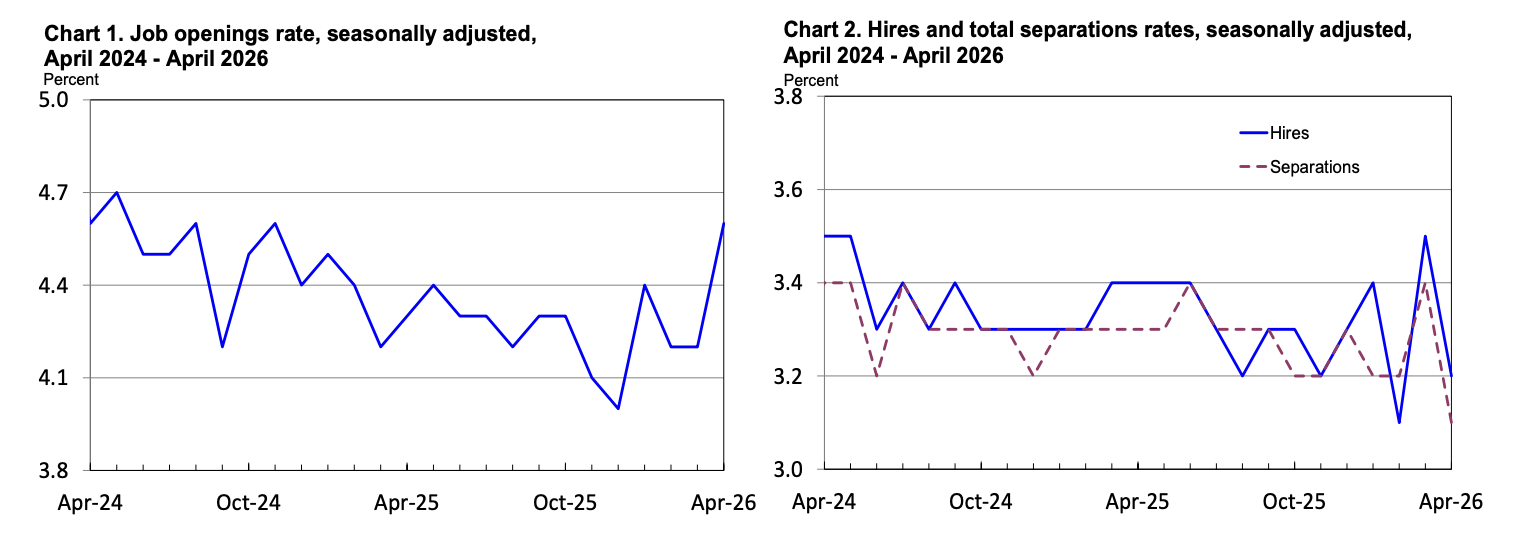

Recent labour market data from the US Bureau of Labor Statistics (BLS) points to a healthy employment environment. The May employment report showed payroll growth of 172,000 jobs, while the Job Openings and Labor Turnover Survey (JOLTS) revealed that job openings increased by 731,000 to 7.6 million in April, the highest level since May 2024. Together, these figures suggest that labour demand remains intact despite stubborn inflation and ongoing geopolitical tensions.

The improvement in hiring conditions follows a period of softer employment data in late February and March. Some of that weakness now appears to have been temporary, driven at the time by severe weather disruptions and the uncertainty

surrounding the outbreak of the Iran conflict on February 28. The rebound in job openings was most pronounced among smaller businesses, which tend to be more exposed to weather-related interruptions.

The broader labour market has also become more balanced. Upward revisions to previous employment reports lifted the three-month average pace of job creation to 188,000 positions per month. The breakeven pace, the number of new jobs needed each month to keep unemployment stable, has also collapsed as immigration has slowed. The St. Louis Fed now estimates it at somewhere between 15,000 and 85,000 jobs a month, down from about 250,000 in 2023. Either way, current hiring levels remain well above breakeven and are consistent with a healthy economy.

Demand Broadens Across Sectors While Hiring Stays Cautious

Sector-level data shows that much of May’s job growth came from leisure and hospitality, private education, healthcare, government employment, construction, and manufacturing. At the same time, some industries experienced weaker demand, including finance, retail, information services and transportation. Job openings increased most strongly in professional and business services, while openings in finance and insurance declined.

Despite stronger labour demand, there are signs that businesses remain cautious. Hiring activity fell to 5.1 million in April even as job openings increased, highlighting that available positions are not always being filled immediately. Voluntary resignations remained steady at 3 million and layoffs stayed relatively low at 1.7 million, indicating that employers are generally retaining workers rather than reducing headcount.

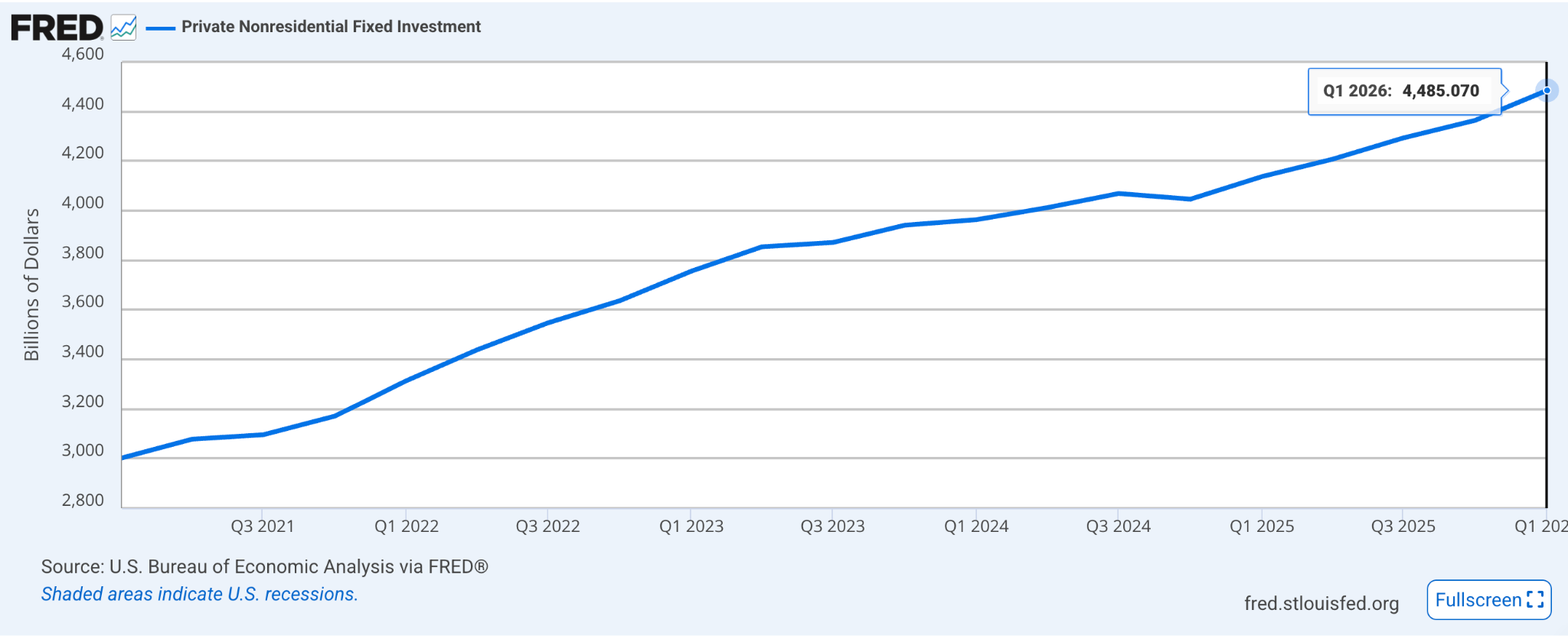

Investment linked to artificial intelligence (AI) infrastructure continues to support economic activity. Large-scale spending on data centres, computing infrastructure and related construction projects has contributed to stronger business investment and rising corporate profitability. Outside construction, however, AI-related employment gains remain limited, suggesting that the technology’s broader impact on hiring has yet to fully materialise.

Inflation Threatens to Outpace Wage Growth

The more significant challenge may come from inflation. Market expectations are centred on a Consumer Price Index (CPI) reading of 4.2 percent year-on-year for May.

CPI measures changes in the prices consumers pay for goods and services and is one of the Federal Reserve’s primary inflation indicators. Higher energy, transportation, fertiliser and food costs are expected to contribute to the increase.

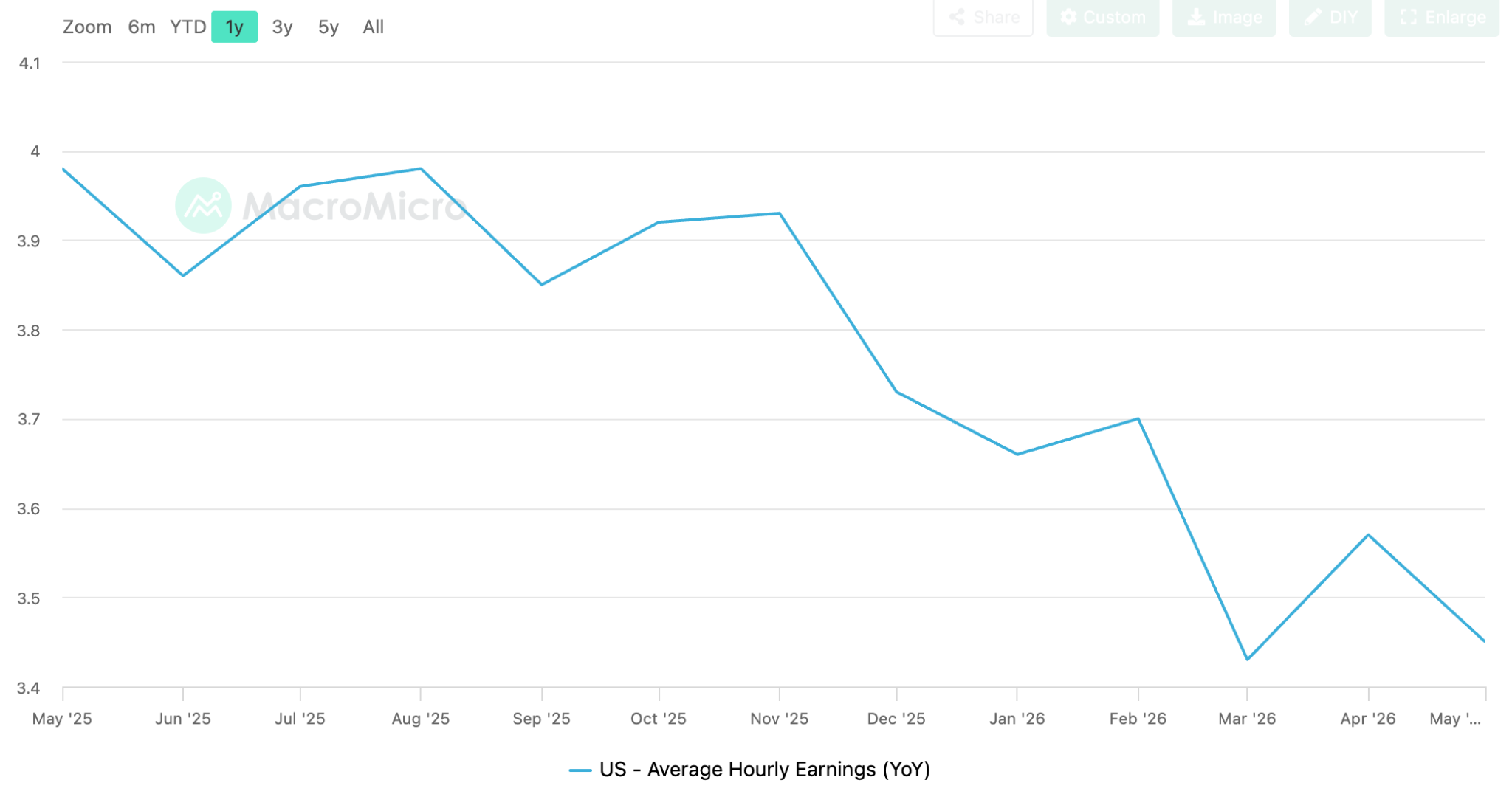

While average hourly earnings rose by 0.3 percent in May and were 3.4 percent higher than a year earlier, inflation is currently rising faster than wages. This means that real wages, which measure earnings after adjusting for inflation, are declining. If inflation remains elevated, households may find that their income buys fewer goods and services despite nominal wage increases.

A Difficult Balance for the Fed

This dynamic creates a difficult policy environment for the Federal Reserve. Under normal circumstances, stable employment and moderate wage growth could support discussions about lowering interest rates. Inflation, however, remains well above the Fed’s 2 percent target, and any further acceleration could force policymakers to maintain restrictive monetary policy or even consider additional rate increases. The real story in the second half of 2026 is not whether the labour market holds, the data says it will, but whether that strength is enough to matter. Resilient hiring, low layoffs and steady business investment are running directly into inflation that is now outpacing wages and eroding real incomes. For households, a strong job market means less when each paycheque buys less. For the Fed, it removes the easy path: stable employment would normally open the door to rate cuts, but inflation well above target keeps that door shut, and any further acceleration pushes policy the other way. The question is no longer whether the economy is strong or weak. It is whether a strong labour market can outrun rising prices, and right now, prices are setting the pace.

Rising Yields and the Oil Shock Tighten Conditions on Risk Assets

The inflation risk is not just an issue for the labour market. It is now setting the price of money across the Treasury curve, and that repricing is the channel through which macro pressure reaches every risk asset, including Bitcoin. Yields are rising for the wrong reason, not faster growth but a higher inflation premium, and risk assets are repricing accordingly.

The Curve Is Repricing Around Inflation, Not Growth

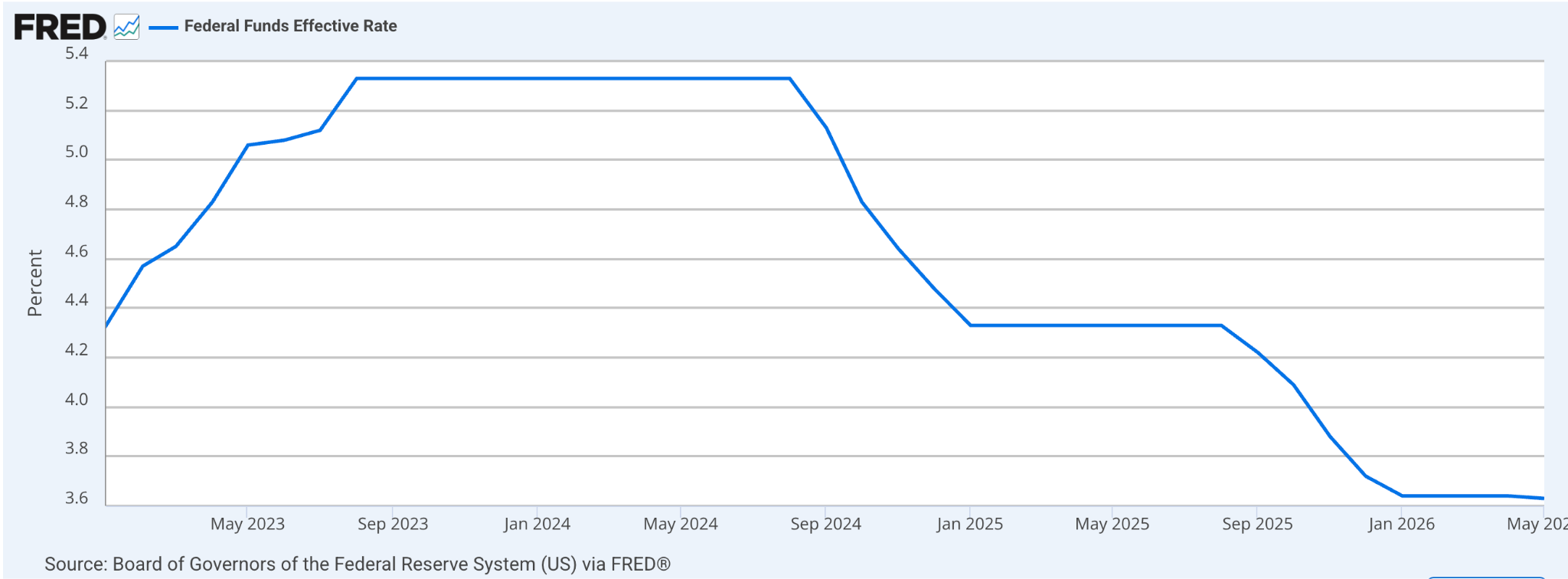

The bond market is telling a clear story in the first week of June, and it is not one of optimism. The yield on the 10-year Treasury note closed near 4.45 percent on 5 June, while the two-year note ended at 4.05 percent. The move followed resilient labour data and a renewed climb in energy costs, a combination that points to firmer inflation rather than stronger demand. The curve remains upward-sloping, with the 10-year trading roughly 38 basis points above the two-year.

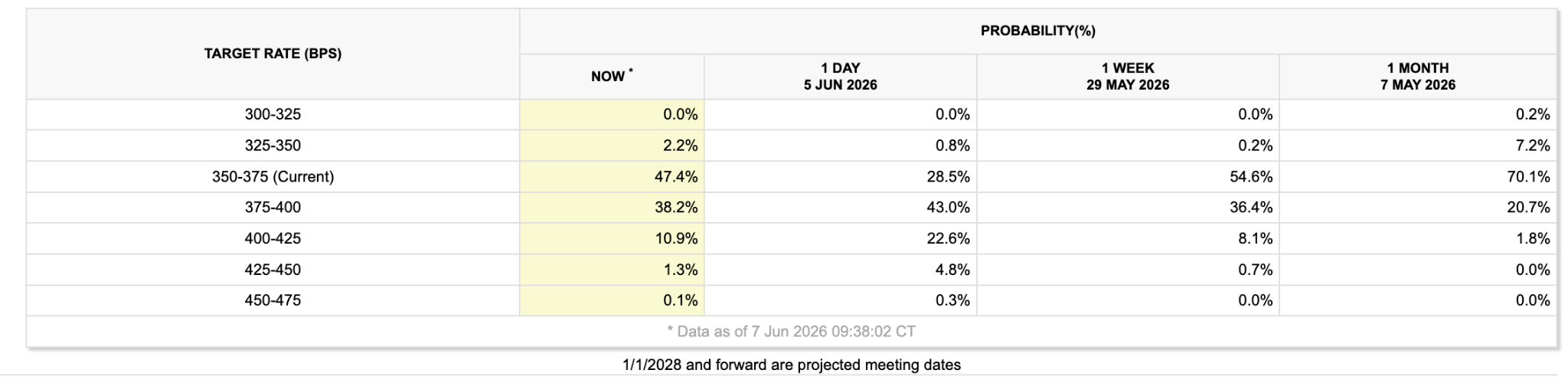

When the front end rises on inflation concern rather than growth, it compresses the room for policy easing. Futures markets now price effectively no change at the Federal Open Market Committee (FOMC) meeting on 16-17 June, and the probability of a rate increase before year-end has edged up to 50.5 percent from 22.5 percent in May. The market is no longer asking when the Federal Reserve will cut. It is pricing the risk that the next move could be a hike.

Real Yields Set the Hurdle for Every Risk Asset

Nominal yields capture the headline, but valuations turn on the real yield, the return left after inflation. The 10-year Treasury Inflation-Protected Securities (TIPS) real yield is sitting above 2 percent, a level that is genuinely restrictive. A higher risk-free real return raises the discount rate applied to future cash flows and lifts the bar that every other asset must clear to attract capital. Assets that generate no yield of their own feel this most acutely.

The catalyst behind the move is energy. Brent crude traded around $93 per barrel and West Texas Intermediate near $91, leaving both roughly three to four percent higher on the week after renewed clashes between US and Iranian forces dampened hopes of restoring flows through the Strait of Hormuz. An oil shock feeds directly into inflation expectations, and rising breakevens push both nominal and real yields higher at the same time. The result is a tightening of financial conditions that the Fed has not engineered and cannot easily offset.

Bitcoin Bears the Brunt as ETF Demand Reverses

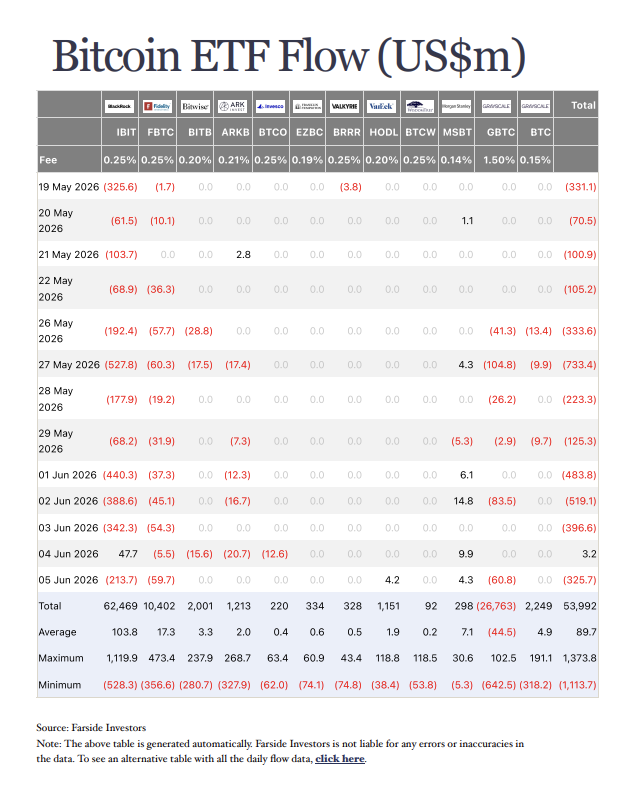

Bitcoin is the clearest expression of this repricing. The marginal buyer over the past 18 months has been the US spot exchange-traded funds (ETF), and that flow is highly sensitive to real yields. As the macro picture shifted, the flow reversed. Over a roughly three-week stretch from mid-May to early June, US spot Bitcoin ETFs recorded net outflows of $3.7 billion, among the heaviest sustained redemptions since the products launched in January 2024.

Price followed the flow. Bitcoin traded under $60,000 on June 6, down close to 28 percent from its mid-May highs above $80,000. The decline lines up precisely with the climb in real yields and the repricing of Fed expectations, which suggests the move is cyclical and macro-driven rather than a structural break in adoption. If real yields top out, the same flow that is leaving can return.

This difficult balance for the Fed now carries a market price. With inflation reaccelerating on energy and the labour market too firm to justify easing, short-term yields stay high and the real yield stays restrictive. This is how the central tension of the second half of 2026 plays out in markets: whether a resilient labour market can outrun rising prices, with the Treasury curve pricing the answer first. Through the back half of the year, risk assets, Bitcoin most visibly, will trade off the path of real yields rather than headline growth. Until the oil premium fades or inflation expectations re-anchor, the burden of proof sits with risk, not with rates.

News From the Cryptosphere

Securitize Clears Final SEC Hurdle for NYSE Listing

On June 5, 2026, the Securities and Exchange Commission declared effective the Form S-4 registration statement covering the merger of Securitize, the BlackRock-backed tokenisation firm, with Cantor Equity Partners II, a special purpose acquisition company, according to the joint filing on the SEC’s EDGAR system. The clearance sets a shareholder vote for June 29, 2026, after which the combined company is expected to begin trading on the New York Stock Exchange under the ticker SECZ. Securitize is the registered transfer agent and tokenisation engine behind BlackRock’s BUIDL fund as well as tokenised products issued by Apollo, KKR, Hamilton Lane, and VanEck. The listing would make it the first dedicated tokenisation-infrastructure provider to trade on a US national exchange.

A Form S-4 is the registration statement the SEC requires whenever a company issues new shares to complete a merger, and the regulator’s declaration of effectiveness is the procedural gate that allows the transaction to proceed to a shareholder vote. The structure here is a reverse merger with a special purpose acquisition company, or SPAC, a publicly listed shell that raises cash in a blind pool and then combines with a private operating business to take it public without a traditional initial public offering. Securitize functions as a transfer agent, the

SEC-registered entity that maintains the official ownership record of a security, except that its ledger is kept on public blockchains rather than in a legacy database. That role places the company at the settlement layer of the tokenised-asset market, which it and its institutional partners have grown to more than $30 billion in issued value.

Strategically, a public listing converts Securitize from a venture-funded infrastructure vendor into a company with exchange-traded equity, giving it acquisition currency, a regulated disclosure cadence, and a cost of capital benchmarked by public markets rather than private rounds. From a market-structure perspective, the more consequential shift is that the plumbing of tokenisation is itself becoming an investable public asset. Until now, allocators seeking exposure to the real-world-asset theme bought the tokens; the SECZ listing lets them own the issuer, transfer agent, and trading venue that the largest asset managers depend on, concentrating a meaningful share of the sector’s settlement activity inside a single regulated reporting entity.

Ultimately, the listing is a marker of convergence, the steady erosion of the boundary between traditional capital markets and on-chain finance. When the firm that tokenises. BlackRock’s funds prepares to ring the opening bell on the same exchange where those funds’ sponsors are listed, the question is no longer whether tokenisation belongs in regulated markets but how much of the existing market it will eventually absorb.

GENIUS Act Comment Window Closes on Stablecoin Rulebook

The public comment period on the federal government’s proposed anti-money-laundering and sanctions rule for payment stablecoin issuers closes on June 9, 2026, one of the final procedural steps before the framework is finalised under the GENIUS Act. The joint proposal issued by the Financial Crimes Enforcement Network and the Office of Foreign Assets Control, dated April 8, 2026 and published in the Federal Register, would treat permitted payment stablecoin issuers as financial institutions under the Bank Secrecy Act. Final regulations are due by July 18, 2026, with full enforcement beginning no later than January 18, 2027.

The GENIUS Act, enacted in 2025, created a federal licensing regime for dollar-backed payment stablecoins and classified compliant tokens as neither securities nor commodities, removing them from the jurisdiction of the SEC and the Commodity Futures Trading Commission. A permitted payment stablecoin issuer, or PPSI, is the licensed entity authorised to mint those tokens. Designating PPSIs as financial institutions under the Bank Secrecy Act, the 1970 statute that underpins US anti-money-laundering law, obliges them to run customer-identification, transaction-monitoring, suspicious-activity-reporting, and sanctions-screening programmes comparable to those of a regulated bank. The proposed rule sets out the specific compliance architecture issuers must build before the enforcement clock starts.

Strategically, the rule raises the fixed cost of operating a compliant stablecoin and favours well-capitalised incumbents that can absorb it, among them Circle, Paxos, and Tether’s domestically regulated USAT, while pricing out thinly resourced entrants. Importantly, it also closes the regulatory ambiguity that kept large banks and payment networks on the sidelines: once the obligations of issuing or handling a stablecoin are written into familiar Bank Secrecy Act language, the compliance question becomes an operational exercise rather than a legal frontier, lowering the barrier for institutions that already run these programmes at scale.

Overall, the closing comment window is a quiet but defining moment in the normalisation of digital-dollar infrastructure. The contest over stablecoins is shifting from whether they will be permitted to the granular work of supervision, reserve standards, and sanctions compliance, the same machinery that governs the rest of the regulated payment system, and that absorption into the ordinary rulebook is precisely what institutional adoption requires.

Bitcoin ETFs Post Largest Outflows Since Launch as Strategy Pivots

Strategy, the world’s largest corporate holder of bitcoin, disclosed on May 26, 2026 that it had repurchased $1.5 billion in principal amount of its zero-coupon convertible notes due 2029 for roughly $1.38 billion in cash, an 8 percent discount to par, and that it held 843,738 bitcoin. The disclosure landed as US spot bitcoin exchange-traded funds were posting their longest and heaviest run of net redemptions since the products launched in January 2024, framing a first week of June in which the institutional bid that powered the cycle visibly cooled.

Strategy’s filing represents a pivot from pure accumulation toward active balance-sheet management. The company retired convertible debt, instruments that can be exchanged for equity, at a discount using cash reserves, while issuing $2 billion of variable-rate perpetual preferred stock and a small tranche of common shares through at-the-market programmes, offerings that sell stock into the open market over time, and used the proceeds to buy 24,869 bitcoin. It also disclosed that its management-designated US dollar reserve, earmarked for preferred-stock dividends, stood at $871 million, and that it now treats the disciplined sale of bitcoin as one capital-management tool among several.

From a market-structure perspective, the simultaneity of record fund outflows and a treasury company restructuring its liabilities marks a maturing of the institutional bid rather than its retreat.

The macro backdrop is doing much of the work: the Federal Reserve’s most recent policy statement, from its April 29, 2026 meeting, kept rates unchanged and described inflation as elevated, in part reflecting higher global energy prices, a higher-for-longer posture that raises the opportunity cost of holding a non-yielding asset. Importantly, redemptions of this kind read more as profit-taking by cycle-early buyers than as a structural exit, while Strategy’s moves show accumulators learning to manage leverage and dividends through a drawdown rather than only adding on the way up.

Ultimately, the week illustrates the maturation of the asset class. A market that once moved only on the size of the next corporate purchase now absorbs a record wave of fund outflows and a balance-sheet reset at its largest holder without structural rupture. It is the behaviour of an asset that has been integrated into institutional portfolios and is now subject to the same macro discipline as everything else in them.