Issue #209:

Iran Truce Lifts BTC as Inflation Tops 4%

Seller Exhaustion Meets a Macro Reprieve

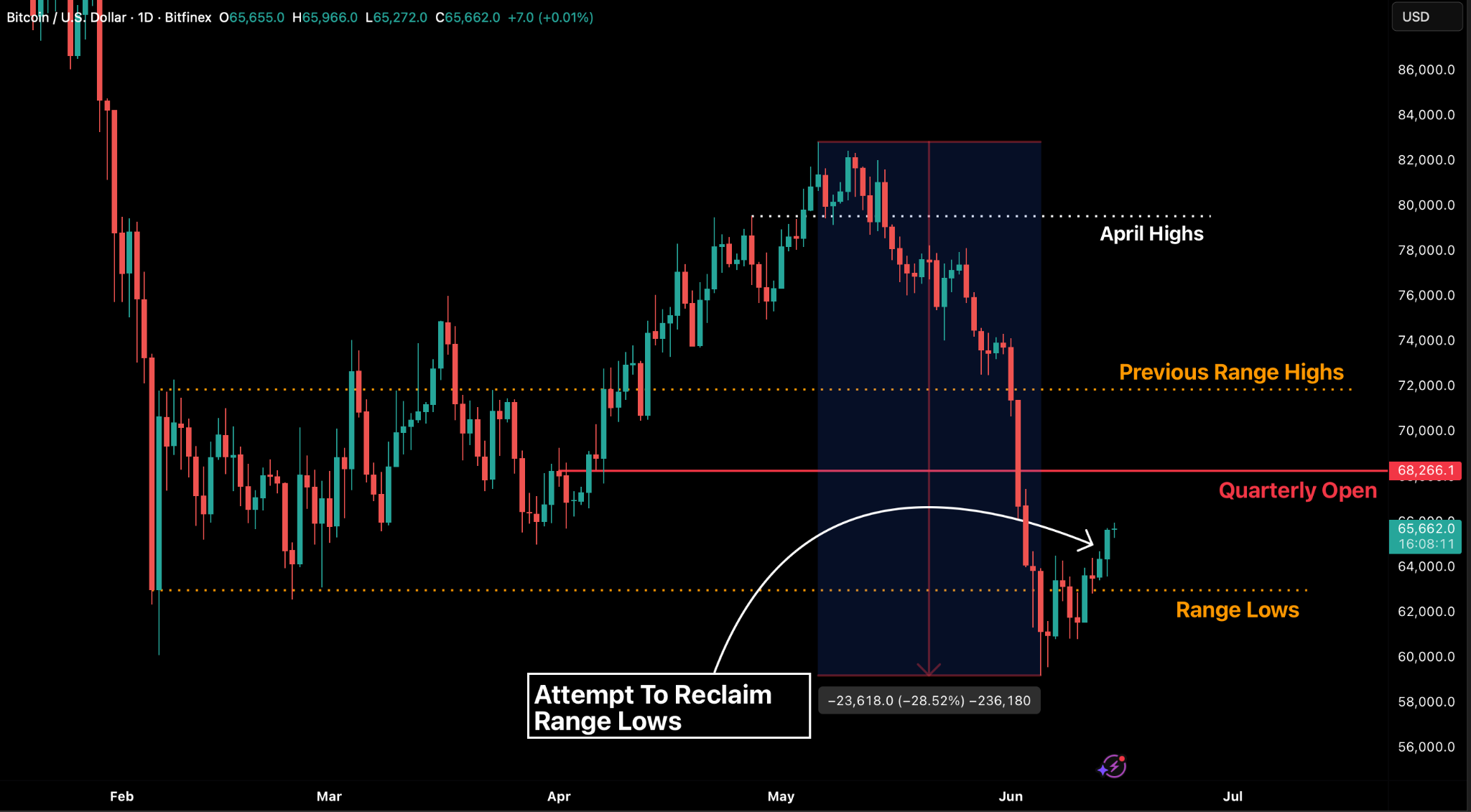

Last week we asked whether there was a floor beneath the floor. This week supplied the answer. The $59,200 low held, price defended the range lows for the third time and Bitcoin closed 3.54 percent higher on the week at $65,655. What lifted the market was seller exhaustion rather than demand. Futures open interest had already been wrung out from its May peak, and short-term holders were capitulating at a loss into a seven-year low in exchange balances.

Beneath the recovery, demand remains the market’s biggest challenge. ETF flows are still negative, treasury-company buying has stalled, and recent buyers remain heavily underwater, with Short-Term Holder profitability metrics showing losses of roughly 17-19 percent. Realised losses continue to accelerate across newer market participants, creating a substantial overhead supply zone.

Price is stuck between two extremes, the cycle floor at the Aggregate Realised Price near $54,000 and overhead supply from Short-Term Holder cohorts where it faces resistance at prices near $68,000 and higher. For now the selling has stopped. The buying has yet to prove itself.

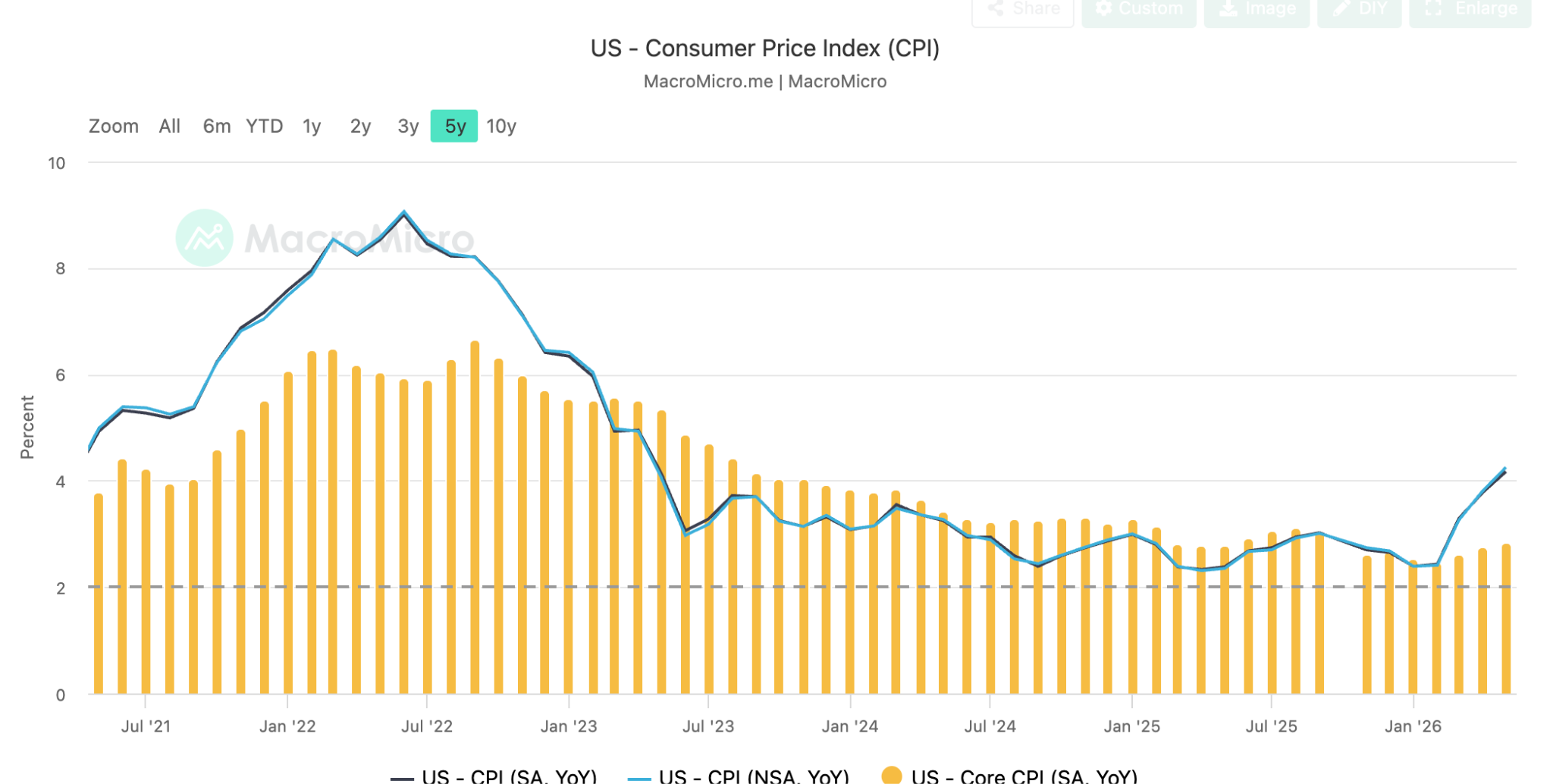

The US macro environment remains dominated by the interaction between inflation, energy markets, and monetary policy. May inflation accelerated to 4.2 percent year-on-year, driven primarily by higher energy costs following disruptions linked to the Middle East conflict. At the same time, economic growth has slowed considerably, with GDP expanding at just 1.6 percent in the first quarter, while real wages continue to decline. This combination of sticky inflation and weakening growth has revived concerns about a mild stagflationary environment.

However, markets have found relief in a proposed US-Iran agreement that would reopen the Strait of Hormuz and ease oil sanctions, potentially removing the supply shock that pushed energy prices higher. If the agreement holds, lower oil prices could ease inflation pressures, reduce real yields, weaken the US dollar, and provide more flexibility for the Federal Reserve as it enters its first meeting under Chair Kevin Warsh.

These macro dynamics continue to shape digital asset markets. A stronger dollar and elevated real yields have weighed on both gold and Bitcoin, reinforcing the view that liquidity conditions remain a more important driver than traditional safe-haven narratives. A sustained decline in energy prices could reverse those pressures and create a more supportive backdrop for risk assets, including crypto. Against this backdrop, institutional adoption continues to deepen. BlackRock has filed for the iShares Bitcoin Premium Income ETF (BITA), a product that combines spot Bitcoin exposure with covered-call strategies to generate yield, signalling the next stage of Bitcoin’s integration into traditional portfolio construction.

Meanwhile, the competition to build regulated digital money infrastructure is accelerating globally. Japan’s three largest banks, MUFG, Mizuho, and Sumitomo Mitsui, have signed an agreement to explore issuing a joint yen-backed stablecoin, highlighting how national financial systems are increasingly moving on-chain to compete with the growing influence of dollar-denominated stablecoins. At the same time, corporate demand for Bitcoin remains strong. Strategy added another 1,550 Bitcoin to its treasury, increasing its holdings to 845,256 BTC and reinforcing the long-term supply absorption trend created by public companies that continue to convert capital market access into Bitcoin accumulation.

Market Signals

Bitcoin Approaching Selling Climax

Bitcoin closed the week at $65,655, 3.54 percent higher than the previous week and as much as 11 percent above the 5 June bear cycle low of $59,200, the lowest level since October 2024. The dynamics behind the current low and the attempt to defend the range lows are more important than raw price data. For now the $60,000 level has held as support for the third time, mainly through seller exhaustion from the primary drivers of the whole decline. This change in order flow happened as the de-escalation in Iran lifted the pressure on oil, yields and the inflation premium. The potential peace deal being signed was a major catalyst over the weekend to solidify a key Q1 2026 range low reclaim near $62,000.

What the tape shows is seller exhaustion arriving at the same moment as a macro reprieve, which is a different condition from genuine demand. The price action that follows each behaves very differently, which leads us to believe that despite the short-term recovery, bulls face significant hurdles before an uptrend can form.

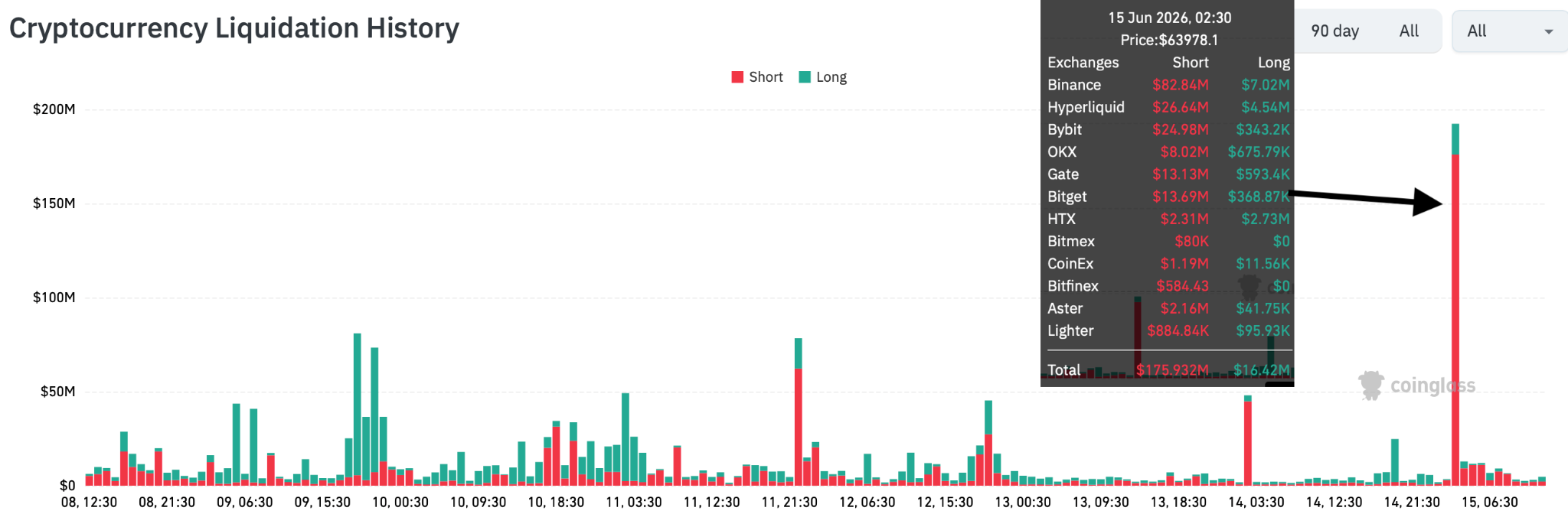

An hour before the weekly futures open, the Iran-US Peace deal announcement came through causing a sharp uptick in BTC moments after the announcement.

BTC drifted 2.5 percent higher within 30 minutes of the move, leading to a positive weekly close. Post which, the move continued and price has remained at the same $65-66,000 level through Asia and London sessions on Monday. This move higher was accompanied by over $176 million in aggregate short liquidations over the same period. Even though open interest has been stagnant after being flushed significantly post our recent move sub-$60,000 in early June, the sticky positioning on the short-side has been punished over the weekend as well.

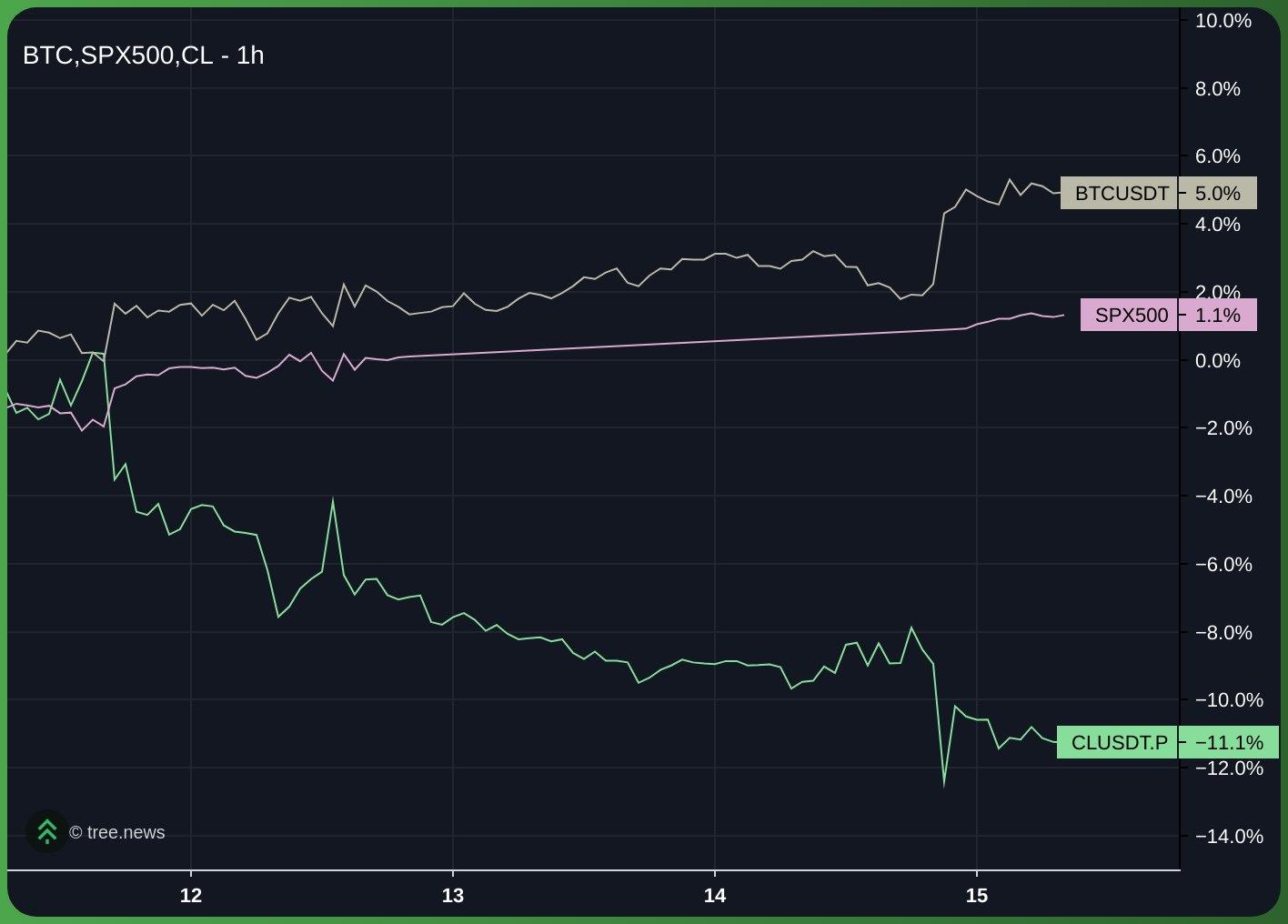

SPX gapped around 0.8 percent higher pre-market since the futures open while BTC has continued in the aforementioned $65-66,000 bracket. Meanwhile, Crude has moved 5.4 percent lower since the peace deal announcement before already having corrected from 94 to the mid 80s since the beginning of June over a series of moves that signalled de-escalation and the anticipation of the peace deal being signed. The June 5th lows in crypto were a front-running of a global meltdown across risk assets where for the first time since 2020, correlations broke down and commodities, equities and yields all drifted lower. The SPX bottomed around June 10 and has already recovered, with an expected move higher on tech stocks and inflation factors like crude oil drifting lower, the market is uniquely positioned for a dovish surprise at the upcoming FOMC this meeting which will also release the first dot plot under new chair Warsh.

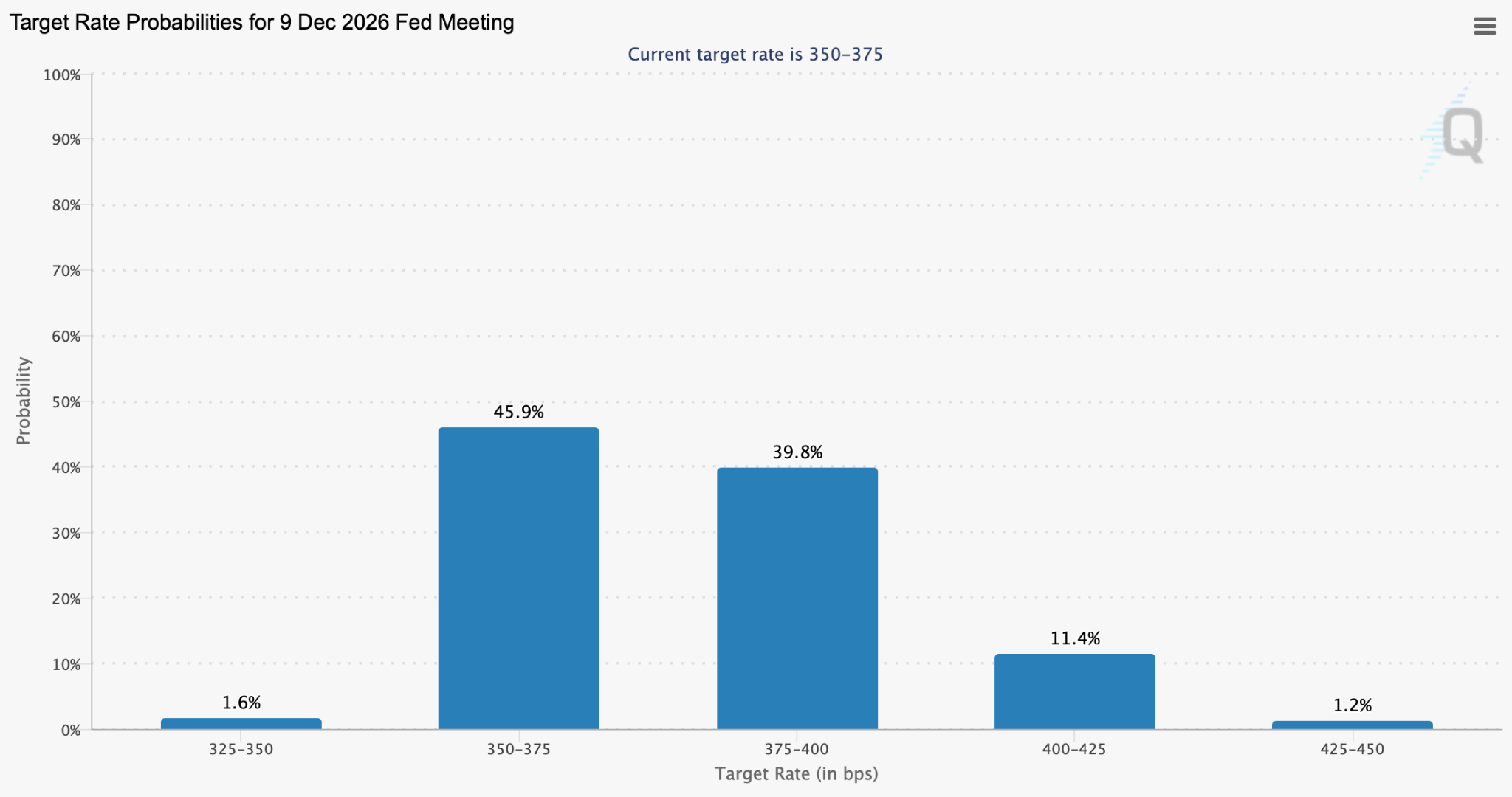

Fed Futures probabilities are still split between rates either being maintained through the end of the year or a potential 25 bps hike but odds of a rate hike have gone down from 43.4 percent to under 40 since the announcement.

We believe that we have a temporary bottom with multiple confluences like correlated assets drifting higher, large liquidations causing a funding and open interest reset and spot seller exhaustion with macro reprieve at the moment. However, the two major spot buyer complexes in ETFs and Treasury/DAT companies need to turn positive for BTC to catch a sustained spot bid. STRC is currently trading at $95.5 on an ex-dividend date, far under the $100 par value. This is the worst STRC performance on an ex-dividend date since launch, with current yields being at 12.1 percent. The ETF outflows have still not reversed despite reducing in intensity. This confirms our thesis: there is an opportunity for a lower-timeframe uptrend, but BTC stays confined to a range until proven otherwise by aggressive spot demand or a reclaim of important pivot levels.

Profitability evaporated when BTC plummeted towards the range lows near $60,000, leaving recent buyers and multiple investor cohorts deeply underwater. Being underwater subsequently triggered a surge in realised losses especially for the Short-Term Holder (STH) cohort. Concurrently, institutional appetite has diminished, treasury acquisitions stagnated, and the options positioning has continued to be defensive across the board.

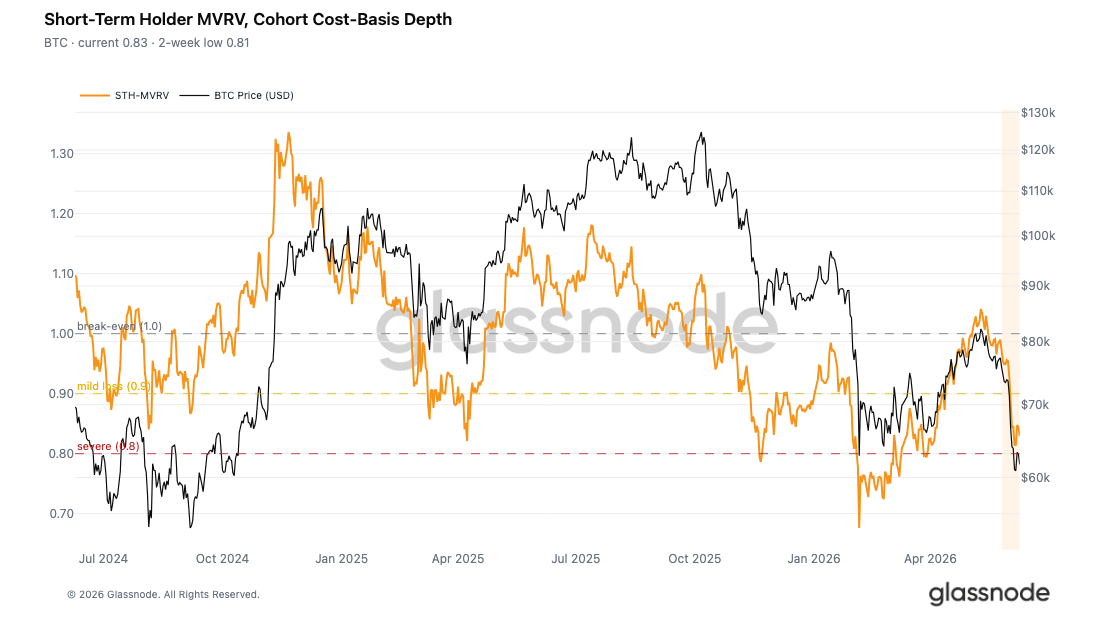

Recent buyer profitability and cost basis typically gives insight into support/resistance levels ahead of time as holders typically tend to re-enter positions or cut them relative to their entry. The Short-Term Holder realised Price (STHRP) via the STH-MVRV shows that this cohort is currently dominated by aggregate unrealised losses.

BTC’s move to range lows sent the metric to 0.81 before slight recovery to 0.83, meaning these investors remain approximately 17 to 19 percent underwater. This data reinforces our previous assessment of how recent buyers are now underwater and this could result in cascading moves lower as more and more of the cohort distributes supply if price moves further below their aggregate entry.

The heavy accumulation cluster (high buying volume observed) between $78,000 and $82,000 from BTC’s range breakout in May is now firmly in the red.

The market is in a transitional phase following new lows that reflects a typical post-liquidation structure, appearing once the primary wave of forced selling from distressed entities exhaust themselves and the tape enters a defensive, wait-and-see phase. Whether this consolidation transforms into a concrete support floor or acts as a temporary pause before another leg lower hinges entirely on the emergence of fresh demand at these price levels.

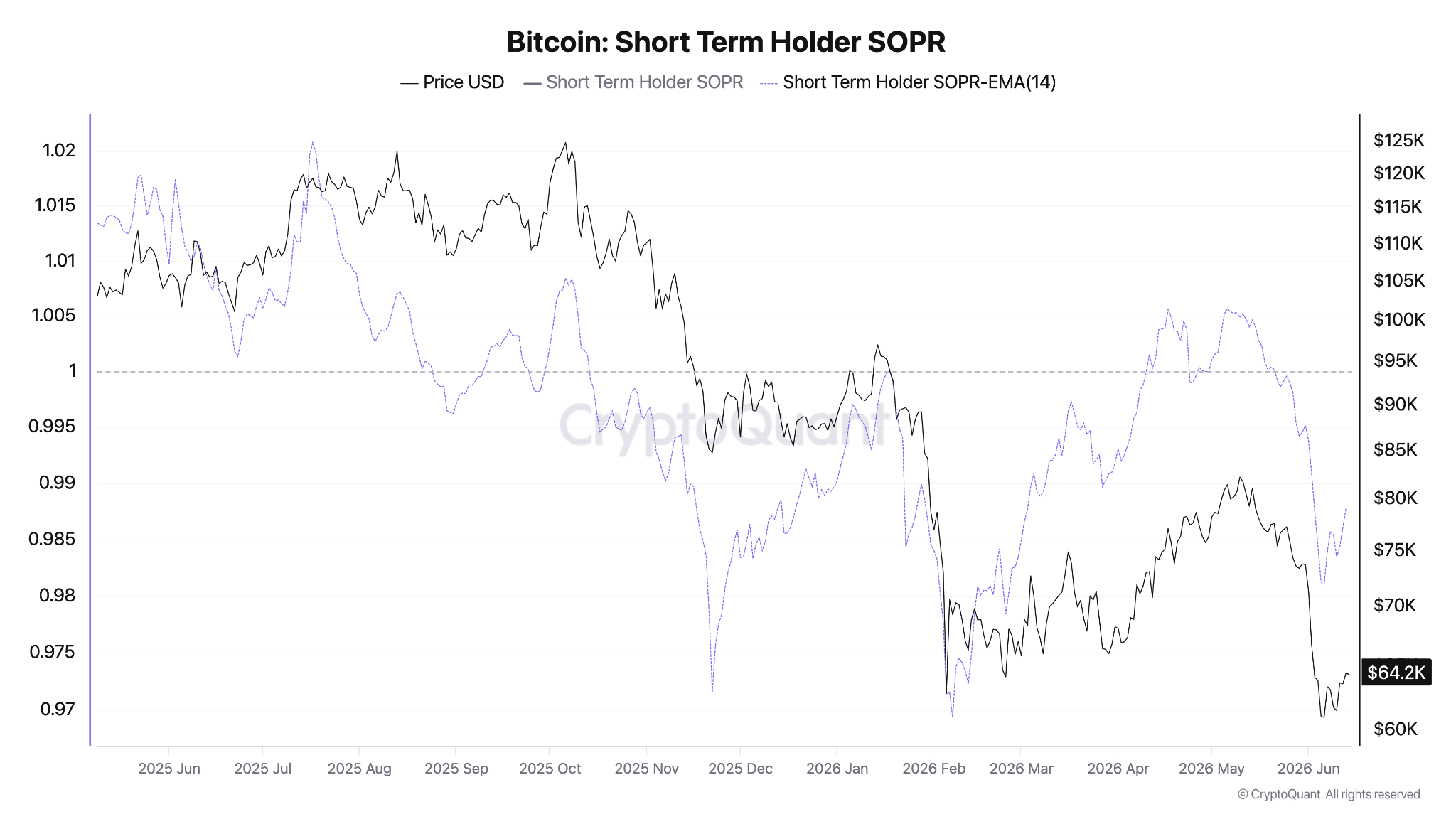

Beyond the landscape of unrealised losses, realised spending behaviour highlights the severity of the current regime. The STH-SOPR (Spent Output Profit Ratio) measures whether short-term holders are moving coins at a profit or loss relative to their acquisition price. This indicator provides a good representation of their cost basis.

Recent buyers are realising losses at an accelerating pace, a trend consistent with the $1.35B in daily realised losses in June’s first trading week and the deeper MVRV signals. Yet, the market remains in a precarious interim: while loss realisation is sufficient to confirm deep-bear conditions, it has not yet reached the intensity historically required to establish a durable, definitive floor. If the STH-SOPR consistently spikes under 0.9 with averages sustaining under 0.96, that typically signals a multi-month bottom which was last observed in February earlier this year.

Our assessment of on-chain dynamics indicates a transition toward late-stage capitulation as opposed to a broader distribution phase. As such, there is constant selling pressure across the previously marginal buyers of BTC like the ETF complex and treasury companies accumulating with respect to NAV premiums, with demand being completely agnostic to price. The STH-SOPR, sustaining under the par value at 1 shows how aggressively recent buyers have turned to sellers once price moved under $75,000.

The infrequent drop of the Long-Term Holder SOPR below 1.0 highlights the current seller exhaustion. Like typical late stage bear market capitulation moves, the LTH-SOPR is holding steady with some infrequent spikes. Overall, the Long-Term Holder total supply is still near ATHs, which implies the SOPR matters less for LTHs than STHs since the overall decline in supply held by the cohort is relatively stable and in a higher timeframe uptrend.

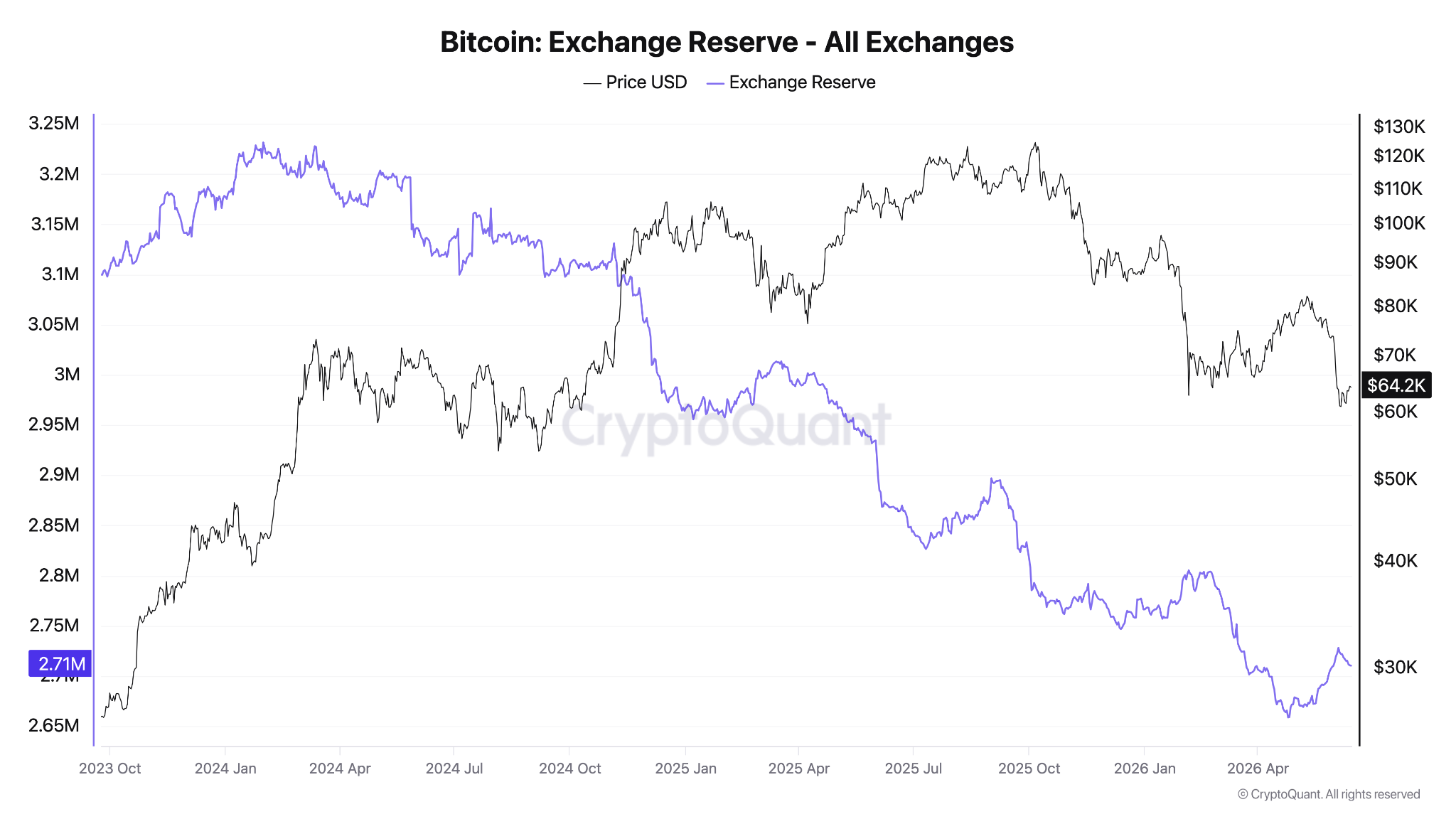

While aggregate supply remains fundamentally resilient, exchange balances are at seven-year lows despite a short uptick during the move under $60,000 in early June before trending lower again, with long-term entities controlling 78 percent of the supply. This transfer from weak hands to strong hands is a necessary condition for establishing a sustainable higher low.

The investor cost-basis map remains our primary structural guide for the immediate outlook. At current spot prices near $65,500, BTC is pinned below the STH cost basis alternating between low-to-mid $70,000s.

Recovery attempts will meet resistance from recent buyers seeking breakeven exits from $68,000 and above if the STH-SOPR remains at the current level. The Quarterly Open at $68,266 adds confluence to that resistance region. Meanwhile, the aggregate Realised Price near $54,000 serves as the definitive cycle floor for the time being for all deeper pullbacks.

Bitcoin is currently trapped in the consolidation zone between these two critical levels, where it must either establish a durable support base or face a potential breakdown into a deeper leg lower.

General Macro Update

The Iran Deal and the Energy Path Ahead

A US-Iran memorandum of understanding scheduled for signing this Friday would reopen the Strait of Hormuz and suspend US oil sanctions, removing the supply trigger behind the recent inflation spike. The deal is partial and reversible, however, which makes the energy path it sets, rather than the headline itself, the real swing factor for rates, the dollar and Bitcoin.

On 14 June, the US and Iran reached a memorandum of understanding to end the war that began in late February, with President Trump and Iranian officials confirming a signing scheduled for Friday, 19 June in Switzerland. Trump has declared the Strait of Hormuz open and ordered the US naval blockade lifted, telling vessels from all nations to sail. The strait carries roughly 20 percent of the world’s seaborne oil, so its reopening is the single largest near-term influence on the energy prices that drove headline inflation above 4 percent in May.

According to Iranian state media, the draft commits Iran to reopening Hormuz within 30 days in exchange for the suspension of US oil and petrochemical sanctions and the release of around half of the 25 billion dollars in frozen assets, with full sanctions relief to be negotiated over a 60-day window. Iran’s missile programme and its relationships with regional proxies are carved out and left unresolved, as is the future of its enriched-uranium stockpile. The official text has not been released and the two governments are publicly pushing differing versions, so the specific terms remain disputed.

The truce is fragile. Fresh Israeli airstrikes on Beirut and exchanges with Hezbollah have already threatened the agreement, prompting President Trump to call for restraint and warn negotiators not to derail it. Senior Israeli officials have said the reported terms endanger their security interests, and the original war aims (regime change, the destruction of Iran’s nuclear and missile capability, and the severing of its proxies) were not achieved. A deal that leaves the most contentious issues for later, and that either side can abandon, is closer to a pause than a resolution. For markets the mechanism is direct. If the truce holds, oil retreats, the energy-led component of inflation fades, real yields and inflation breakevens ease, and the dollar’s safe-haven bid unwinds. That same chain is the clearest near-term tailwind for gold and Bitcoin, both of which have traded this cycle as non-yielding, dollar-sensitive assets pressured by macro liquidity rather than supported by any safe-haven narrative. The risk is binary: a collapse back into conflict would re-close Hormuz, spike crude and reinstate every pressure the deal is now relieving.

The timing sharpens the signal. The agreement lands the day before the Federal Open Market Committee meets on 16 and 17 June, the first meeting chaired by Kevin Warsh. A credible supply normalisation gives the Committee cover to treat May’s spike as transitory and hold, rather than tighten into a headline print above target. The sections that follow trace how this single event runs through the rest of the macro picture, first the May inflation print it helped drive, then the dollar and real-rate signal that prices gold and Bitcoin. For now the Iran deal is the upstream variable, and whether Friday’s signing holds and Hormuz traffic actually normalises is what the rest of the articles hinges on.

Inflation Reaccelerates: Energy Shock And Policy Uncertainty Cloud The Outlook

Rising energy costs are once again driving inflation higher in the US, while uncertainty surrounding the Middle East conflict continues to shape market expectations for interest rates and economic growth. The picture has shifted sharply in recent days, with the US-Iran agreement detailed in the opening article now set for signing on Friday. Persistent price pressures and weakening household purchasing power suggest inflation risks have not yet fully passed through the economy, but the deal raises the prospect that the energy spike behind this print begins to reverse, even as a fragile truce keeps the path two-sided. The Consumer Price Index (CPI), released by the US Bureau of Labor Statistics (BLS), rose 0.5 percent in May, pushing annual inflation to 4.2 percent, in line with the forecast outlined in the previous Bitfinex Alpha report. This marked the first time inflation has exceeded 4 percent since May 2023. The increase was largely driven by higher energy-related costs, including gasoline, transportation and airfares. Core inflation, which excludes food and energy, remained comparatively moderate at 2.9 percent year-on-year.

The gap between headline and core inflation is important. With core running at 2.9 percent against a 4.2 percent headline, the acceleration is concentrated in energy rather than broad-based across the economy. That distinction shapes the policy response. An energy-led spike can fade quickly if supply normalises, whereas a rise in core pressures would prove far stickier. Timing matters too. The May data reflects the onset of the conflict, Operation Epic Fury, rather than the more recent June hostilities, whose effects will appear only in later prints. That normalisation is now in view: the Hormuz reopening and the suspension of oil sanctions would remove the supply driver behind the May spike, though the prints already in the pipeline will stay elevated before any relief shows through.

However, the latest data indicates that the early energy impact is already spreading through the broader economy. Energy prices rose 23.5 percent over the past year, while gasoline prices increased 40.5 percent. Higher transportation and utility costs are now affecting a wide range of goods and services, increasing costs for households and businesses alike.

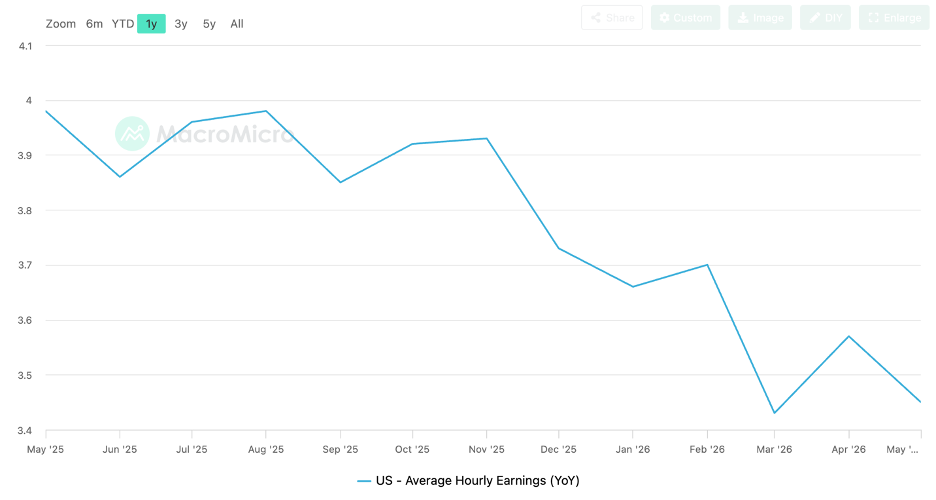

A key concern is that wage growth is no longer keeping pace with inflation. Real average hourly earnings, which measure income after adjusting for rising prices, declined 0.1 percent month-on-month in May and 0.8 percent over the past year. When real wages fall, households can afford fewer goods and services even if their pay rises in nominal terms. This trend could weigh on consumer spending during the second half of the year, particularly among lower-income and middle-income households.

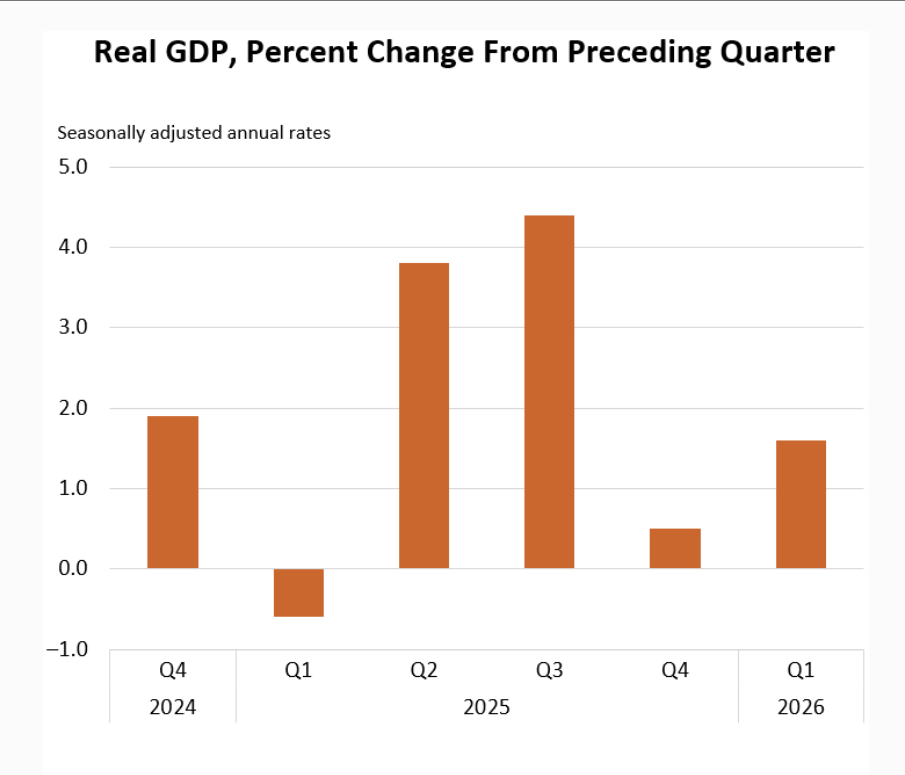

The growth side of that picture has now turned as well. Real GDP expanded at an annualised 1.6 percent in the first quarter of 2026 and just 0.5 percent in the fourth quarter of 2025, a marked step down from the 3.8 percent and 4.4 percent pace recorded in the second and third quarters of last year. Output is still expanding, but the two most recent quarters have averaged around 1 percent, less than a third of the mid-2025 rate, even as inflation has accelerated. That pairing of cooling activity with firming prices is what gives the stagflationary characterisation its second leg, the growth slowdown that the inflation and real-wage data alone could not establish.

Such a backdrop, in which inflation stays firm even as growth momentum and household demand soften, is the textbook definition of a mild stagflation, and it is the most difficult environment for a central bank, because the two halves of its mandate, stable prices and maximum employment, begin to pull in opposite directions.

Financial markets, however, are focusing on the easing of geopolitical tensions. With the US-Iran agreement set out in the opening article now scheduled for signing on Friday, equity indices have moved higher and oil prices have retreated from recent highs. That relief is real but fragile, leaving markets exposed if the truce unravels before the supply picture normalises.

Attention is now turning to the upcoming Federal Open Market Committee (FOMC) meeting on 16 and 17 June, the first chaired by Kevin Warsh. Markets assign near-certain odds to rates being left unchanged, so the more important signal will be the guidance. Policymakers are widely expected to drop their previous bias toward easing in favour of a neutral stance, and any hawkish language would indicate continued concern about inflation. The timing matters: a credible supply normalisation arriving the day before the meeting gives the Committee cover to treat the energy spike as transitory and hold, rather than respond to a headline print above 4 percent with tighter policy.

The bond market is already signalling expectations of tighter-for-longer conditions, with the 10-year Treasury yield trading around 4.5 percent. The base case is higher for longer rather than imminent hikes. However, if energy-driven inflation broadens or geopolitical tensions re-escalate, pressure for an outright rate increase later this year would build, and a hawkish surprise at Warsh’s first meeting would reinforce that risk. Conversely, if the truce holds and oil continues to retreat, the energy premium embedded in yields should fade, pulling the curve back toward the easing path markets had priced before the conflict.

The combination of rising inflation, declining real wages and ongoing geopolitical uncertainty creates a challenging backdrop for policymakers. While the diplomatic resolution now taking shape has supported financial markets, the underlying inflation picture remains fragile. Unless energy prices continue to moderate and supply-side pressures ease, inflation is likely to remain above the Federal Reserve’s target, limiting the central bank’s flexibility in the months ahead. The deal is the clearest route to that easing, but until it is signed and Hormuz traffic actually normalises, the risk stays two-sided.

A Strong Dollar And Falling Gold: The Real-Rate Signal That Matters For Bitcoin

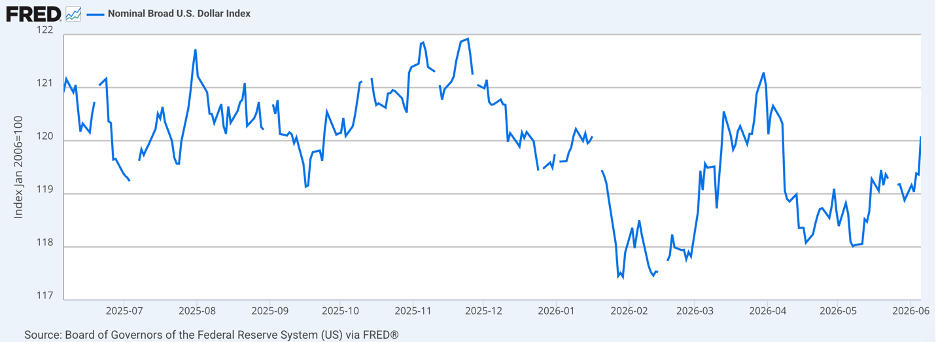

A stronger dollar and elevated real yields are pressuring gold and Bitcoin at the same time. This is a sign that macro liquidity, rather than the safe-haven narrative, is currently setting the price for both. The energy shock is the trigger, but the cross-asset signal is where the forward risk shows up. With a US-Iran truce now scheduled to be signed on Friday, that forward risk has turned two-sided: a holding deal that pulls oil and real yields lower would remove the very pressure weighing on both assets. Since the outbreak of hostilities, the dollar has appreciated despite ongoing concerns surrounding US fiscal policy, trade uncertainty and inflation. Investors have once again treated the dollar as a preferred safe-haven asset during a period of geopolitical instability.

Gold, traditionally viewed as a store of value during periods of uncertainty, has moved in the opposite direction. After recording strong gains between 2022 and 2025, gold prices have weakened considerably since the conflict began. The primary driver is dollar strength. A firmer dollar mechanically pressures dollar-priced gold and absorbs the safe-haven flows that might otherwise support bullion. Reinforcing this, the return of inflation concerns has kept interest rates and real yields elevated, raising the opportunity cost of holding a non-yielding asset such as gold.

The same real-rate and dollar dynamics extend to Bitcoin, which trades as a non-yielding, dollar-sensitive asset and has likewise struggled to gain traction during the dollar’s advance. In a strong-dollar, high-real-yield regime, both gold and Bitcoin face headwinds, which suggests that for now macro liquidity conditions matter more for each than their respective safe-haven narratives. That logic cuts both ways. If the Iran truce holds, oil retreats and the inflation premium fades, real yields and the dollar’s safe-haven bid should ease, and the same macro-liquidity channel that has pressured Bitcoin would turn into its strongest near-term tailwind. Markets are also beginning to reprice inflation risk directly. Longer-term market-based inflation expectations have firmed as energy costs feed through, and rising expectations are precisely what the Federal Reserve fears, because they can become self-fulfilling once embedded in wage and price-setting behaviour.

With the Strait of Hormuz set to reopen as described above, the supply disruption that was not in view when the May data was collected is now starting to clear. Even so, the prices already in the system will take time to unwind: the May CPI captured the onset of Operation Epic Fury, gasoline still sits above pre-conflict levels, and the renewed exchanges in early June will surface only in later prints. As in the energy shocks of the 1970s and after Russia’s 2022 invasion of Ukraine, higher fuel costs feed through with a lag, so the lagged inflation already in train and the durability of the truce, rather than the temporary retreat at the pump, are what the dollar and real-yield signal now hinges on.

The resilience of the US dollar also highlights the challenges facing efforts to reduce global reliance on the currency. While several countries have sought to diversify reserves and promote alternatives to the dollar, recent market behaviour suggests that investors still view the dollar as the most liquid and reliable destination during periods of economic stress. That safe-haven premium, however, is partly a function of the conflict, and a durable truce would likely unwind some of it, easing the very dollar strength that has weighed on gold and Bitcoin. Energy, currency and commodity markets are pointing the same way: inflation risks may re-emerge later this year even if fuel prices temporarily retreat. With the supply picture now turning on whether the truce holds, and investors still favouring the US dollar for the moment, the broader environment remains vulnerable to renewed price pressures should the deal falter.

News From the Cryptosphere

BlackRock Files for a Bitcoin Income ETF

On 9 June, 2026, BlackRock filed an amended Form S-1/A registration statement with the Securities and Exchange Commission for the iShares Bitcoin Premium Income ETF, an actively managed fund set to trade on Nasdaq under the ticker BITA at a sponsor fee of 0.65 percent. The fund holds spot Bitcoin alongside shares of BlackRock’s existing iShares Bitcoin Trust (IBIT) and writes call options on a portion of those holdings each month, converting Bitcoin’s volatility into a recurring income stream for holders.

Per the registration statement, the trust seeks to generate premium income by selling (writing) covered call options on IBIT shares and on indices that track spot Bitcoin products, typically against 25 to 35 percent of its holdings each month. A covered call is an options strategy that collects an upfront premium in exchange for capping the upside above a set strike price. The structure caps participation in sharp rallies while delivering monthly distributions, a trade-off familiar from equity income funds now ported onto a digital asset. At 0.65 percent, the sponsor fee undercuts existing covered-call Bitcoin products, positioning BITA as a low-cost entrant in a category that did not exist at institutional scale a year ago.

The filing extends the Bitcoin ETF complex beyond simple spot exposure into structured yield, the same progression that equity markets underwent as plain index funds gave way to buffered and income overlays.

From a market-structure perspective, an income wrapper widens the addressable buyer base to mandates that require cash flow, including pensions, endowments and retiree-income allocations that cannot hold a non-yielding asset. The competitive dimension is equally significant: BlackRock is racing comparable products from rival issuers toward a near-term launch, and a registration nearing effectiveness signals that trading is weeks away rather than quarters. BITA reflects the capital-markets engineering that now defines Bitcoin’s institutionalisation. Each new wrapper, from spot funds to options-based income vehicles, embeds the asset deeper into the machinery of traditional portfolio construction, normalising Bitcoin as a standard building block that asset managers package and distribute like any other exposure.

Japan's Megabanks Sign a Joint Yen Stablecoin Pact

On 10 June, 2026, MUFG Bank, Mizuho Bank and Sumitomo Mitsui Banking Corporation announced in a joint press release that they had signed a memorandum of understanding (MOU) to jointly examine the issuance of a yen-denominated stablecoin, with the aim of conducting live commercial transactions during fiscal year 2026, which ends in March 2027. The three institutions are Japan’s largest banking groups, and the agreement commits them to a shared council studying the operational, governance and technical frameworks for issuance.

According to the announcement, the stablecoin would be issued under a trust structure in which the three banks act as joint settlors and a licensed trust bank serves as trustee, a model that keeps reserves bankruptcy-remote from the issuers. The trust-based design aligns with Japan’s revised Payment Services Act, which has permitted licensed banks and trust companies to issue stablecoins under regulatory supervision, giving the project a clear legal pathway that is absent in many jurisdictions.

A bank-issued yen stablecoin lets the three lenders defend their position in payments and settlement against both private stablecoin issuers and overseas dollar tokens that dominate the market. The move mirrors a broader contest in which national banking systems are racing to put regulated, currency-denominated tokens on-chain before dollar-backed stablecoins entrench themselves as the default settlement layer for tokenised finance. Importantly, a consortium model spreads the cost and standard-setting across the incumbents rather than ceding the rails to a single challenger.

The agreement is a marker of the jurisdictional competition now shaping tokenised money. As the United States advances its own stablecoin framework and dollar tokens expand abroad, Japan’s megabanks are moving to ensure the yen has a regulated, institutional presence on-chain, a reminder that the contest to define digital money is increasingly being waged between sovereign financial systems, not just private firms.

Strategy Adds 3,137 BTC to Its Treasury

On 15 June 2026, Strategy disclosed in a Form 8-K filing with the Securities and Exchange Commission that it had acquired 1,587 BTC for $100 million, at an average price of $63,024 per coin, during the period from 8 to 14 June. The purchase lifted the company’s aggregate holdings to 846,842 BTC, bought for a cumulative $64.07 billion at an average price of $75,656. In the week prior as per a filing on 8 June, the company had added 1,550 BTC.

The purchases deepen their treasury model. It allow the conversion of equity-market access into a standing bid for Bitcoin, with each issuance-funded buy removing coins from circulation and into long-term corporate custody. This absorption matters most when it coincides with exchange-traded fund outflows, since it provides an offsetting source of structural demand independent of the ETF channel. The trade-off is that the strategy concentrates the firm’s balance sheet in a single volatile asset, leaving its equity premium sensitive to swings in Bitcoin’s price and to investor appetite for fresh share issuance.

Strategy raised $209 million through sales of MSTR common stock under its at-the-market programme, yet directed only $100 million of that into BTC while channelling a near-equal sum into its USD Reserve, lifting that balance to $1.1 billion. Notably, no Stretch (STRC) preferred shares were sold during the period, the variable-rate vehicle that has anchored much of the firm’s recent funding produced zero proceeds. The firm appears to be prioritising liquidity to service debt and dividend obligations over maximising coin accumulation. The USD Reserve’s stated mandate, backstopping preferred dividends and debt interest, frames the decision plainly: in a week of soft preferred demand, cash took precedence over Bitcoin.

For the supply-absorption thesis, this matters more than the headline holdings figure. The treasury bid is not unconditional; it flexes with the firm’s ability to raise capital cheaply through its preferred and equity channels, and with the competing claim on cash from its dividend obligations. When appetite for instruments like STRC softens, accumulation slows and a larger share of any proceeds is retained as reserve rather than converted into coins.